What is a Utility Token? Utility Tokens Explained

December 28, 2023 - 11 min read

Utility Tokens Serve Multiple Purposes Within Blockchain Ecosystems

A utility token is a blockchain-based asset that serves a specific purpose within a protocol, platform, or ecosystem. Utility tokens can be utilized for various purposes, including DAO voting, allowing access to a particular system or feature, like swapping cryptocurrency on a decentralized exchange, providing rewards, or tipping individuals on a blockchain-based social network. This contrasts with regular cryptocurrencies like Bitcoin and Ethereum, which generally act as a store of value.

In addition to regular cryptocurrencies, utility tokens are often compared to security tokens, which provide ownership rights in a company or protocol. However, many tokens and cryptocurrencies have utility and represent ownership in a company or protocol, meaning that this distinction can sometimes become unclear.

Utility Tokens vs. Security Tokens and Equity Tokens

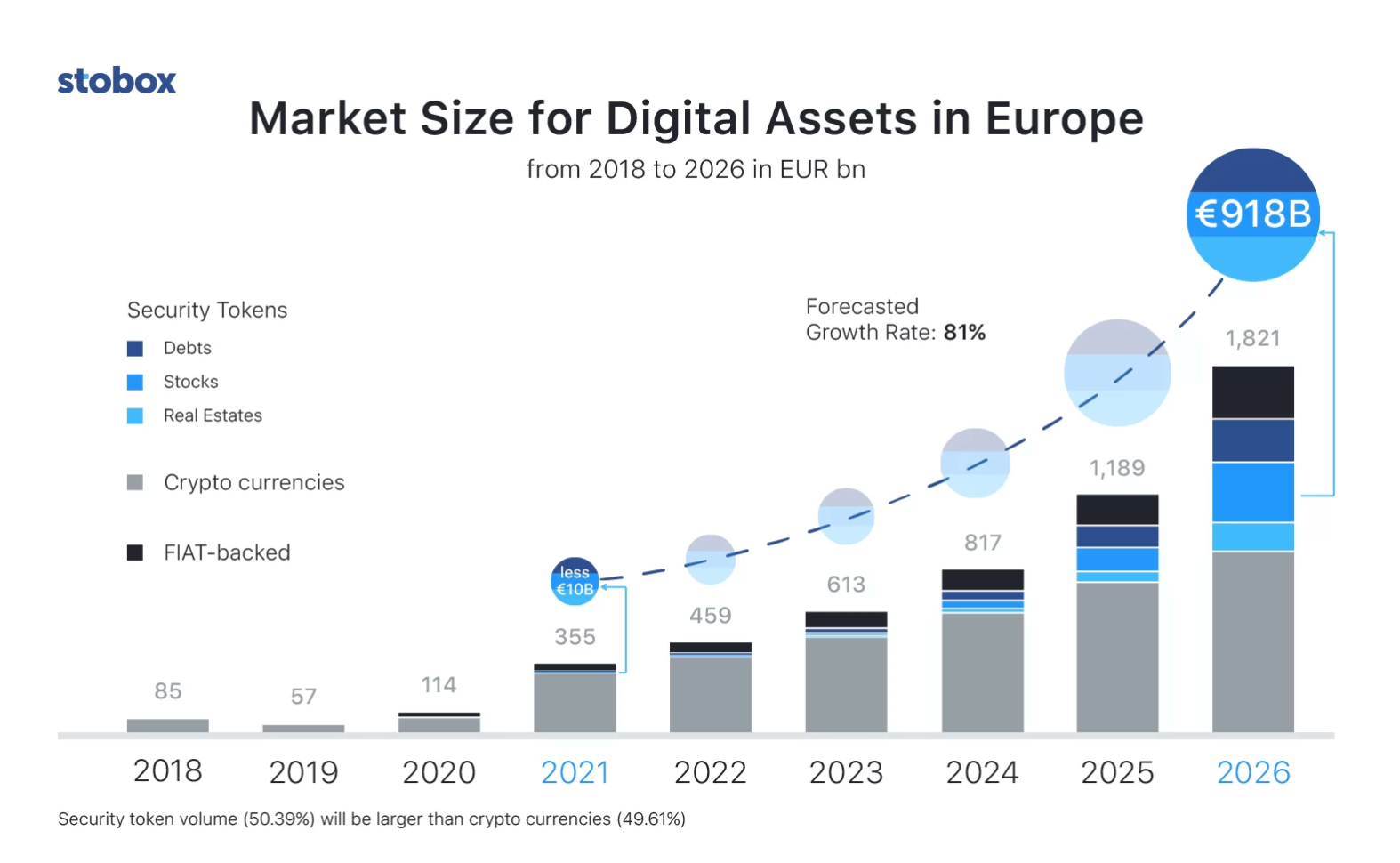

Digital assets market size projection (Europe), 2018-2026, including security tokens. Source: The Tokenizer.

While utility tokens are digital assets with specific uses, such as voting or governance, security tokens represent ownership of external assets. These could include shares in a company, real estate, or other similar assets. Unlike utility tokens, which are generally unregulated or regulated as commodities (like Bitcoin and Ethereum), security tokens, at least in the United States, are subject to laws that govern traditional securities, like stocks, bonds, mutual funds, and ETFs. When security tokens specifically represent shares in a company, they may also be referred to as equity tokens.

It should be noted that a security token can also provide significant utility to users, but this does not make it a utility token.

Howey Test diagram. Source: SEC/Crypto News.

In order to be regulated as a security instead of a utility token or a commodity, a crypto asset must pass the Howey Test. The Howey Test defines a security as:

- A type of “investment contract.”

- An investment contract is defined as an “investment of money in a common enterprise with a reasonable expectation of profits to be derived from the efforts of others.”

- The owner of the investment contract “is led to expect profits solely from the efforts of the promoter or a third party.”

So, for a cryptocurrency to be classified as a security or a security token:

- “An investment of money

- In a common enterprise

- With the expectation of profit

- To be derived from the efforts of others.”

It should be noted that security tokens are different than cryptocurrencies that are simply labeled by the SEC as securities. Security tokens, unlike cryptocurrencies simply classified as securities, are initially formed with the intention of being classified as securities.

Security tokens can be legally issued through a variety of federal laws, including:

- Regulation A: Issuing securities through Regulation A allows the issuer to accept up to $50 million in investment from the general public. However, setting up an investment vehicle that compiles with Regulation A can be relatively time-consuming.

- Regulation S: This regulation allows U.S. entities to issue securities outside the United States legally, provided they follow the financial and securities regulations of the country where they will issue the securities.

- Regulation D: Issuing securities through Regulation D means the issuer does not have to pre-register with the SEC. However, they must prove that they have only issued securities to accredited investors and that they have not issued any false or misleading statements.

- Regulation Crowdfunding: The JOBS Act of 2017 allows companies to sell up to $5 million of their securities to the public via regulated crowdfunding platforms without specifically registering with the SEC.

Security tokens can be issued on various blockchains, including Ethereum. Currently, Ethereum has two security token standards, the ERC-1400 standard and the ERC-3643 standard. ERC-3643 tokens offer a more centralized model, as they contain an automated validator system that allows for identity verification and permits the issuer of the securities to control the tokens and their transfers. In contrast, the ERC-1400 standard allows each token trade to be validated by a unique key generated off-chain.

In theory, ERC-20 fungible tokens and ERC-721 and ERC-1155 NFTs can also be used as security tokens, though they are not specifically designed or optimized to do this.

Utility Tokens for DAO Voting and Governance

As previously mentioned, utility tokens can play a core role in DAO governance. Many major DeFi protocols, like Uniswap and MakerDAO, are governed by DAOs in a one-token, one-vote system that allows token holders to vote on governance proposals. For projects on the Ethereum blockchain, most of these tokens are ERC-20 tokens.

However, soulbound tokens (SBTs), NFTs that cannot be transferred from wallet to wallet, are increasingly being used as utility tokens for DAO voting. This helps replace the one-token, one-vote system with a fairer, more equitable “one-person, one-vote” system, which reduces the power of whales who often dominate the DAO voting process, leading to a significant degree of DAO centralization. SBTs on the Ethereum blockchain are most commonly issued using the ERC-5114 token standard.

For example, the increasingly popular Ethereum Layer-2 Optimism already uses SBTs as part of its two-house DAO governance system, with one of the governance houses using a traditional one-token, one-vote system and the other utilizing SBTs for a “one-person, one-vote” governance system.

Examples of Utility Tokens

Basic Attention Token (BAT) logo. Source: Basic Attention Token.

Below are a few examples of popular utility tokens:

- Binance Coin (BNB): This token is generally utilized to pay for trading fees and transactions on the Binance exchange. Users can get discounts by paying their fees in BNB instead of other cryptocurrencies.

- Uniswap (UNI): Uniswap is the most popular DEX (decentralized exchange) on the market today. The exchange operates by incentivizing users to stake their tokens in order to provide liquidity for traders, and, as a reward, these stakers (sometimes referred to as liquidity miners) are compensated in UNI tokens.

- Basic Attention Token (BAT): This is the native token of the Brave browser, which can be used by advertisers and is also issued by Brave as a reward for users watching advertisements on the browser.

Stablecoins as Utility Tokens

DAI stablecoin logo. Source: Chain Debrief.

By providing a stable form of cryptocurrency that can be used as a store of value and a stable exchange mechanism/settlement layer, stablecoins provide significant utility to the crypto and blockchain ecosystem, and most centralized exchanges would not be able to operate effectively without them. Therefore, stablecoins can be considered utility tokens while not solely used for utility purposes.

Different forms of stablecoins can provide slightly different types of utility, with centralized, 1:1 dollar-backed (and dollar redeemable) stablecoins like USD Coin (USDC) providing the highest level of stability, and more decentralized stablecoins, like DAI, providing a higher level of autonomy to crypto users. For example, while USDC holders have a much stronger guarantee of currency stability, DAI holders can be assured that potential governmental and regulatory crackdowns will have much less impact on their ability to transact effectively.

Asset-Backed Cryptos as Utility Tokens

Much like stablecoins, cryptos backed by real-world assets, like gold, can function as stores of value and utility tokens, as they provide an easy way for investors to get exposure to highly-desired commodities like gold. Popular gold-backed tokens include PAX Gold (PAXG), Tether Gold (XAUT), and Gold Coin (GLC).

NFT Utility Tokens

BAYC Otherside game screenshot. Source: The Mediaverse.

In addition to fungible tokens, NFTs can provide users with significant utility. Some common forms of utility provided by NFTs include:

- Royalty Sharing: Royalty-sharing NFTs have become increasingly popular in the last few years, with various musicians funding concert tours by selling NFTs that guarantee the holders a portion of the tour’s revenue or profit. Royalty-sharing NFTs can also be used by other creatives, like visual artists, to provide NFT holders a certain portion of the revenues created by each sale or transfer of the NFT to a new wallet.

- DAO Voting: As previously reviewed, NFTs, particularly soulbound tokens (SBTs), play an increasingly influential role in DAO voting.

- Community Access and Rewards: A variety of extremely popular NFT projects, including the Bored Ape Yacht Club (BAYC), have added community access and rewards as an additional utility for their token holders. For instance, BAYC holders can sometimes gain access to exclusive parties and events. Other rewards offered by many NFT projects include access to future NFT projects, airdrops, and metaverse events.

- Ownership of Real-World Assets: Another utility provided by certain NFTs is ownership of real-world assets, like wine or real estate. Sometimes, these tokens may be classified as security tokens, and other times, as utility tokens. In many cases, these tokens are created as fractional NFTs, meaning that a single NFT represents full ownership of the asset, such as a house or a bottle of expensive wine. However, in this case, the NFT is effectively broken into many individual pieces. This means that each fractional NFT owner effectively owns a small fraction of the underlying asset.

Utility Token Issues and Concerns

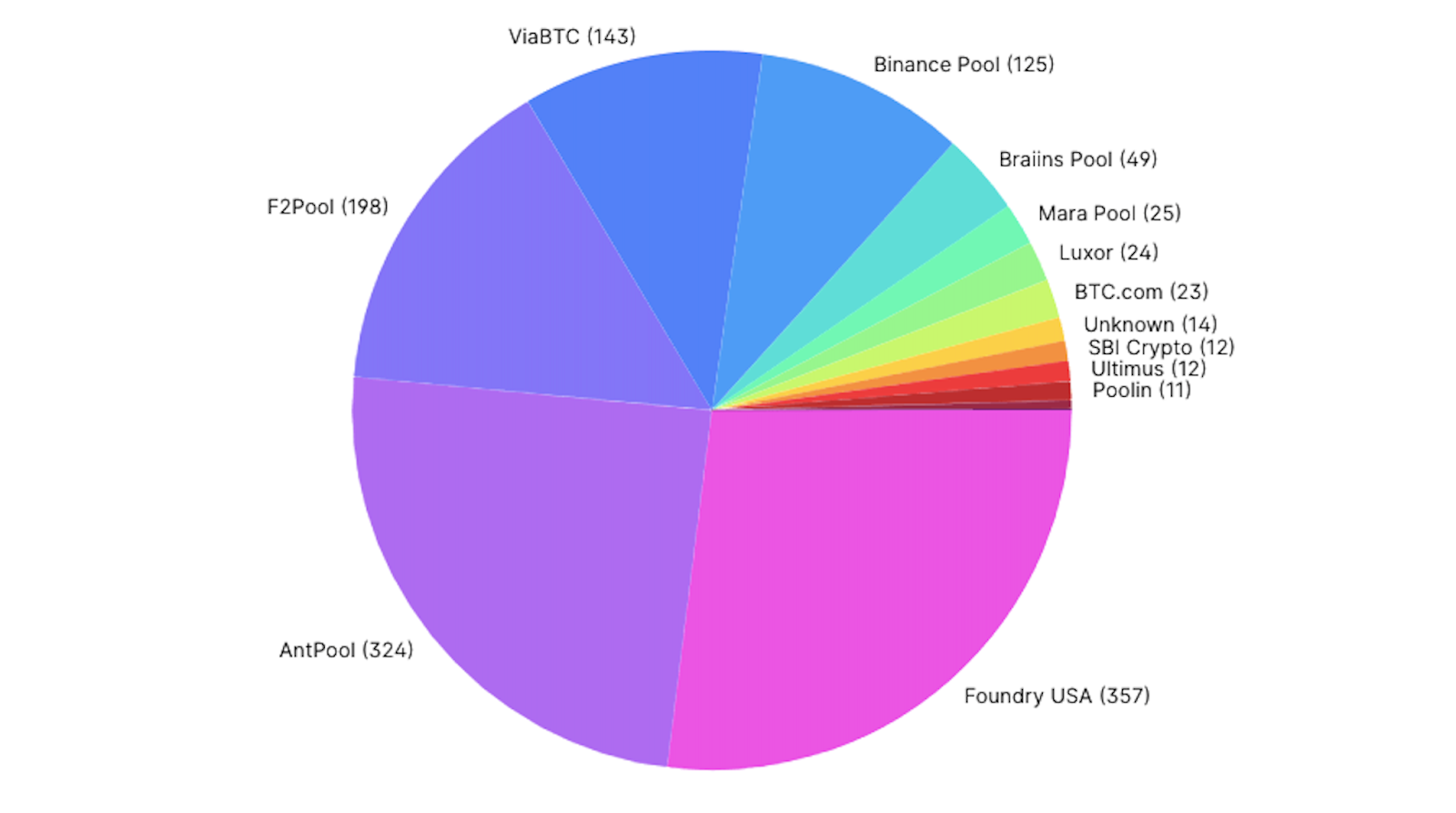

This Bitcoin hashrate pie chart shows AntPool and Foundry USA as representing more than 51% of Bitcoin’s total hashrate (Jan. 2023). Source: CryptoSlate.

While utility tokens are essential to the blockchain and crypto industry, they aren’t perfect. Some common issues involving utility tokens include:

- Transaction Fees: Since pure utility tokens are designed to serve a purpose, not just serve as a store of value or an investment, some find it concerning that many tokens, especially tokens on Ethereum (like ERC-20 fungible tokens and ERC-721 and ERC-1155 NFTs) carry high transaction fees, especially during times of high network congestion. While it’s true that Ethereum fees have generally trended downward recently, they have spiked to incredibly high levels in certain scenarios. For instance, during the Bored Ape Yacht Club (BAYC) NFT mint, minting fees sometimes cost thousands of dollars, and a record $175 million of ETH was wasted during failed minting transactions.

- Scams and Rug Pulls: Just like other cryptocurrencies, projects involving utility tokens aren’t immune to scams and rug pulls. This can include rug pull NFT projects, in which the project’s creators hype it up, promising lots of utility and generating significant interest around the project. This often leads to an initial price spike during the initial minting process, but in these situations, the founders quickly abandon the project and essentially ‘run off’ with the money. In addition, NFT projects aren’t full rug pulls, but they do overpromise the utility of their NFTs (such as promising merchandise and community access to real-world or metaverse events) without actually providing the merchandise or events in practice. Also, scammers sometimes create fake tokens that resemble a project’s utility tokens but are fake, rendering them worthless and without any utility. This can often happen when users transact on smaller decentralized exchanges (DEXs) that may have less stringent security protocols.

- Regulatory Uncertainty: As discussed earlier in this article, most “utility tokens” do actually have some (if not all) elements of securities and, at the very least, act as a store of value of some kind. This means that projects that issue these tokens could face legal action, and the holders of these tokens may have difficulty selling them if they’re delisted from exchanges or other punitive actions are taken. If enough utility token users have difficulty transacting with their tokens, this could significantly reduce liquidity and potentially impact token holders’ ability to engage in DAO voting.

- Centralization: Centralization is a major concern for all blockchain and crypto projects that want to promote decentralization– from major cryptos like Bitcoin and ETH to smaller start-up projects. For instance, while it’s true that cryptos like ETH have major utility– providing a way for users to pay fees that allow them to use thousands of dApps, the majority of ETH staking is controlled by only a few staking pools. For example, many believe that the staking protocol Lido controls too much of the staked ETH on the Ethereum network, potentially giving it too much voting power and undue influence on the overall Ethereum ecosystem. Bitcoin is potentially even more centralized, with the top two mining pools consistently providing more than half of the entire hashrate of all Bitcoin miners worldwide.

Conclusion: Many Tokens Provide Utility, But Regulations Are Still Unclear

As discussed earlier in this article, many currently classify tokens as security or utility tokens. However, the truth is that many tokens blur the lines between both classifications, providing some form of ownership in a shared enterprise and significant utility.

As previously mentioned, there should also be a significant distinction made between tokens that are initially issued as security tokens registered with the SEC and cryptocurrencies and tokens that were initially issued as cryptocurrencies but are not classified as securities by the SEC. Security tokens often have to go through some form of approval process and often require users to go through a KYC (know-your-customer) process in order to invest in the token. Like traditional cryptocurrencies, security tokens can be issued on any blockchain.

In contrast, tokens classified as only utility tokens generally do not pass the Howey test, as they are decentralized to a sufficient degree that there is no “common enterprise,” and individual investors cannot expect to gain profits by the “work of others.” This is primarily why Bitcoin and Ethereum have been classified as commodities by the Commodities Futures Trading Commission (CFTC) rather than being classified as securities by the SEC.

With the SEC increasingly cracking down on cryptocurrencies, we may see many more utility tokens being classified as securities. Therefore, we can expect many more crypto projects to initially issue security tokens registered with the SEC rather than to independently issue cryptocurrencies via private initial coin offerings (ICOs) or initial DEX offerings (IDOs).

However, this mainly applies to tokens issued in the United States, as the SEC generally does not have much international jurisdiction, except when serious issues arise involving U.S. citizens or corporations.

We also expect the creators of fungible tokens and NFTs to increasingly offer more utility to users as a way to increase investment and community engagement, particularly in NFT projects. Soulbound tokens (SBTs) also represent a sea-change in blockchain identity verification and DAO voting and will likely continue to provide significant utility across a wide range of projects.

References:

- Nibley, B. (Dec. 2021) What Is a Utility Token? SoFi.

- Reiff, N. (Jul. 2023) Howey Test Definition: What It Means and Implications for Cryptocurrency. Investopedia.

- Regulation Crowdfunding. Investor.gov (Securities and Exchange Commission)

- ERC-3643 vs ERC-1400. Tokeny.com.

- (May 2022) ERC-5114: Soulbound Badge. Ethereum Improvement Proposals.

- Gubadze, D. (Apr. 2023) What Are Utility Tokens And How Do You Use Them? Stack.

- (Oct. 2023) Top 6 Gold Backed Cryptocurrency For 2023 [Updated List] Software Testing Help.

- Mcshane, G. (Nov. 2022) What Are Utility NFTs? CoinDesk.

- Rhodes, D. (May 2022) Otherside Digital Land Sale — $175M In Transaction Fees Wasted. Medium: The Green Light.

- Wilser, J. (Sep. 2023) Does Lido Control Too Much Liquid Staking? CoinDesk.

RECENT POSTS

Get news, insights, and more

Sign up for the Supra newsletter for news, updates, industry insights, and more.

©2026 Supra | Entropy Foundation (Switzerland: CHE.383.364.961). All Rights Reserved