CBDC Wallets, Explained

December 03, 2023 - 11 min read

Much Like Crypto Wallets, CBDC Wallets Allow Individuals and Institutions To Spend CBDCs

CBDC wallets are government or bank-issued blockchain wallets that allow individuals to spend and transfer central bank digital currencies (CBDCs). CBDC wallets are similar to crypto wallets but generally only enable users to spend one specific CBDC.

Popular examples of government-issued CBDC wallets are China’s digital yuan wallet app, Nigeria’s eNaira wallet, and the DCash CBDC wallet, which is currently used by a group of Caribbean countries, including Antigua and Barbuda, Grenada, Saint Christopher (St Kitts) and Nevis, Saint Lucia, Saint Vincent and the Grenadines, and Anguilla.

In contrast, countries with multiple bank-issued CBDC wallet options include India, The Bahamas, and Jamaica.

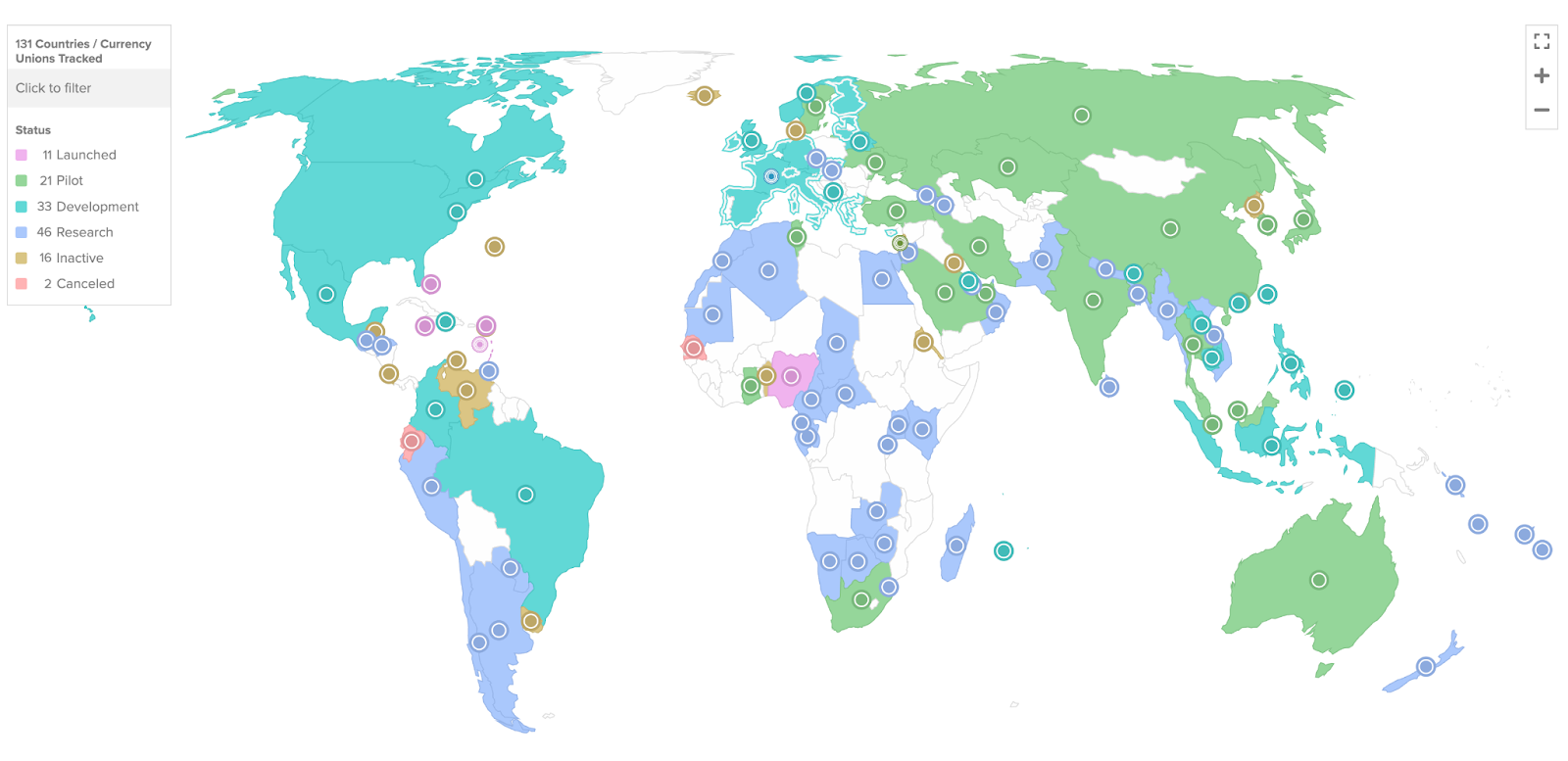

CBDC global adoption map, Sep. 2023. Source: Atlantic Council.

Government-Issued vs. Bank-Issued CBDC Wallets

As we just mentioned, there are generally two types of CBDC wallets: government-issued (i.e., central bank-issued) CBDC wallets and bank-issued CBDC wallets. Each type of wallet has potential benefits and drawbacks. For example, government-issued CBDCs can likely be rolled out faster. In addition, they may be more secure, as only one software system needs to be changed when the wallet rolls out new cybersecurity updates or user features.

Government-issued CBDC wallets could facilitate easier government benefits transfers to citizens, particularly for government payments such as social security, disability, welfare and food stamps, government pensions, and other similar payments. This could make it easier for people to get their funds faster and more securely while increasing transparency and reducing fraud and mismanagement of funds.

However, government-issued wallets could make it even easier for governments to track user transactions, which has already been a major concern for privacy and global human rights advocates. In addition, having only one wallet could severely limit innovation, as only the government could roll out new features.

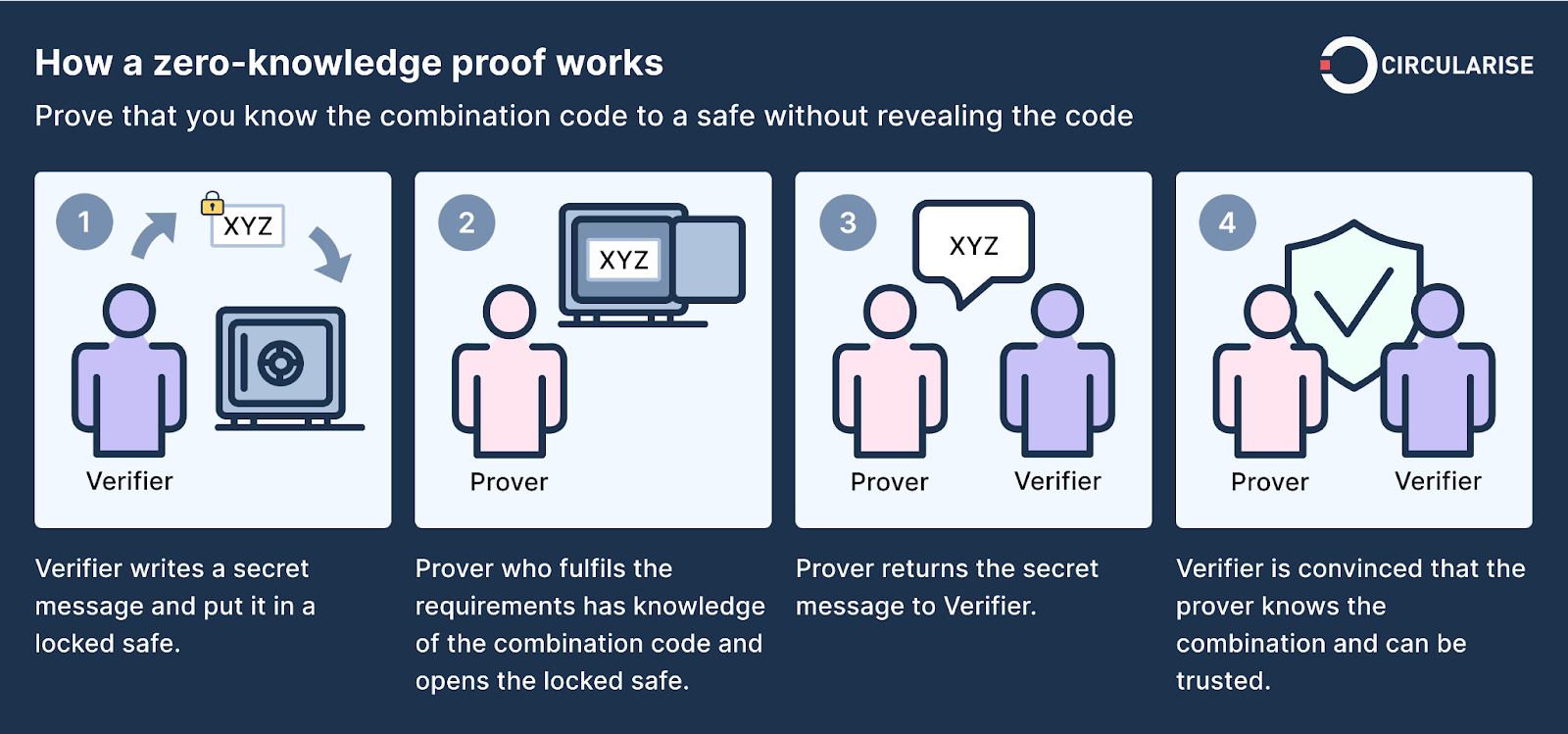

Zero-knowledge proof explanation flow-chart. Source: Circularise.

In contrast, bank-issued CBDCs could compete for users, leading to more innovation, better features, and even better security (though that part is debatable). Private banks, in collaboration with central banks, may also offer better privacy features, such as blockchain IDs concealed via cryptographic proofs (like zero-knowledge proofs or ZKPs).

These cryptographic proofs could prove that a real person who has undergone a stringent KYC (know your customer) review process has sent a specific amount of money to another account but would not reveal the individual’s real-world identity. With a strict legal structure intended to protect user privacy, each bank could have “back-door” access that would allow them to reveal the individual user’s identity, but only for “compelling reasons” such as an official, court-ordered search warrant. This could allow governments to track crime without significantly infringing on privacy rights (or at least not infringing on them as much as a central-bank-issued wallet would). While this system might still have many issues, it could be a step above a fully government-created CBDC, particularly when it comes to user privacy.

Countries With Government-Issued CBDC Wallets

Below, we’ll review several of the most prominent countries with government-issued CBDC wallets:

China

China’s digital yuan (e-CNY) mobile wallet app. Source: Fintextra Research.

Many consider China’s digital yuan CBDC project to be the largest and most successful CBDC pilot program to date, with over 260 million users. As early as January 2022, China’s pilot e-CNY app, created by the People’s Bank of China’s (PBOC’s) digital currency research institute, could be downloaded in Chinese Android and Apple app stores in cities including Shanghai. The e-CNY app is currently connected to most of the country’s largest state-owned banks, as well as some of the largest private banks, such as WeBank (partially owned by Tencent) and MyBank (partially owned by Ant). Other banks must currently rely on interfacing and partnering with these larger banks in order to access the e-CNY app.

As of September 2023, the e-CNY app had gone through nearly 25 updates, with the latest update allowing for additional mobile payment transfers and utility bill payments customized for individual cities.

In addition to widespread adoption by major banks, the e-CNY wallet has been integrated into around 140 merchant platforms, including online retailers like Taobao, JD.com, and Vipshop, as well as ridesharing apps like Didi. These integrations are likely one of the major factors that helped the Chinese CBDC wallet expand to more than a quarter-billion users. QR-code functionality is also in the trial phase, which could lead to additional users and CBDC payment enablement for more major payment rails, like WeChat Pay, Alipay, and UnionPay QuickPass.

Nigeria

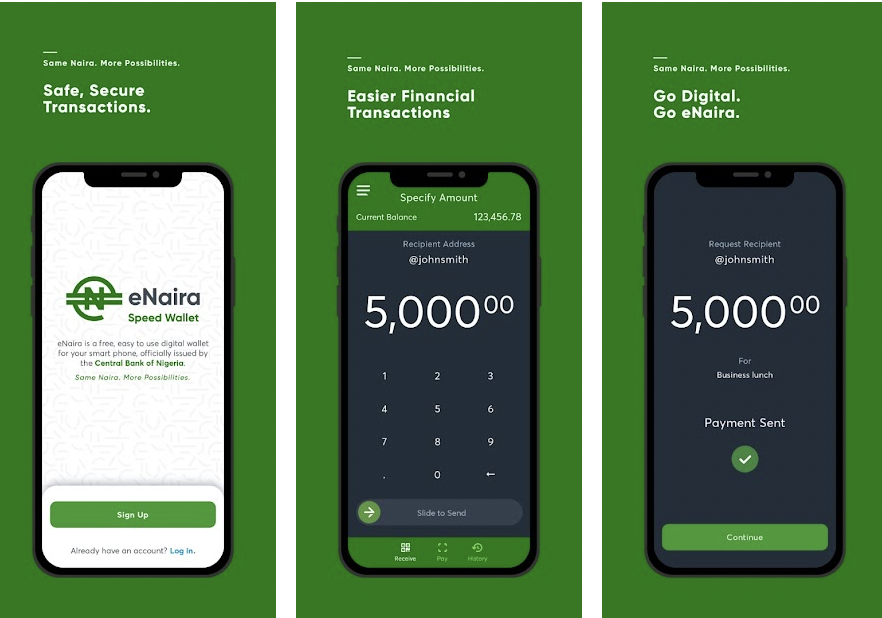

Phone views of Nigeria’s eNaira CBDC wallet. Source: Fintech Blueprint (Substack).

Nigeria is another early adopter of CBDC technology, with its CBDC, the eNaira (and the associated eNaira wallet) being released in October 2021, making it the second country with a fully-functioning, publically available CBDC, only preceded by the Bahamian SandDollar.

Currently, the eNaira wallet can only be accessed by individuals with a traditional bank account. However, the Central Bank of Nigeria (CBN) plans to eventually allow anyone with a mobile phone to create their own CBDC wallet. This could help improve financial inclusion and would have a major impact on Nigeria’s large unbanked population, which is currently estimated to be nearly 40 million people (or more than one-third of the country’s adults). Eventually, the country’s central bank hopes that 90% or more of the country will utilize the wallet.

The eNaira and the eNaira CBDC wallet are also expected to help facilitate remittances, typically consisting of payments sent back to Nigeria by Nigerians working abroad. These remittances reached $24 billion in 2019, meaning that they have a substantial impact on the Nigerian economy and the purchasing power of many ordinary Nigerian families. However, these remittances generally come with exorbitant fees, with some remittance fees as high as 7%. In contrast, remittances done through the eNaira wallet would be free of charge (or nearly free of charge), particularly if the Nigerian government can successfully partner with international money transfer operators to facilitate this process.

Finally, the Nigerian government hopes that the eNaira will help the government trace more transactions (particularly ones that were previously made informally), expanding the tax base, and improving overall transparency.

The Eastern Caribbean Central Bank (ECCB)

The Eastern Caribbean Central Bank (ECCB) DCash CBDC wallet. Source: DCash.com.

While not associated with a single government, The Eastern Caribbean Central Bank (ECCB) is an international central bank that guides the monetary policy of the Organisation of Eastern Caribbean States (OECS), an intergovernmental union consisting of Antigua and Barbuda, the Commonwealth of Dominica, Grenada, St. George’s, Montserrat, Saint Kitts and Nevis, Saint Lucia, and Saint Vincent and the Grenadines. Associate members of the OECS include Anguilla, the British Virgin Islands, Guadeloupe, and Martinique.

The ECCB’s CBDC project, DCash, and the associated DCash wallet have been formally adopted by Antigua and Barbuda, Grenada, Saint Christopher (St Kitts) and Nevis, Saint Lucia, Saint Vincent and the Grenadines, and Anguilla. DCash was another one of the earliest CBDCs to launch, with its pilot program officially beginning in March 2021. Similar to the CBDC ecosystem in Nigeria and China, the DCash wallet is currently the only wallet that users can utilize to transact with DCash.

Countries With Bank-Issued CBDC Wallets

Below, we’ll review several of the most prominent countries with bank-issued CBDC wallets:

India

Yes Bank CBDC wallet for digital rupees. Source: Yes Bank.

As of July 2023, the Reserve Bank of India (RBI) stated that 13 banks participated in its retail CBDC pilot. Their CBDC, called the Digital Rupee, is currently in the pilot program stage, with slightly more than 1 million users and more than 260,000 merchants participating in its program. India’s pilot program has each participating bank issue its own CBDC wallet. In the near future, these wallets will likely be linked to the RBI’s Unified Payment Interface (UPI), an increasingly popular payment system.

The RBI hopes that CBDC users will eventually be able to obtain a wallet without a bank account, which could increase financial inclusion in a country where it’s estimated that up to 700 million people (around half of the country’s population) have little to no access to the traditional banking system.

The Bahamas

SandDollar CDBC wallet. Source: SandDollar (The Central Bank of the Bahamas).

The Central Bank of the Bahamas SandDollar digital currency has been one of the most successful and advanced CBDC projects in North America. However, like most other CBDC projects, it’s still in its pilot stage. In May 2023, it was announced that SandDollar-enabled wallets could access the Bahamas Automated Clearing House (ACH) system to help further link these wallets to the traditional financial system. Their 2.0 wallet, which would allow users to self-active their wallet, is currently in testing.

Currently, mobile SandDollar wallet users can utilize third-party transfer functions within their traditional online and mobile banking applications to send funds to their SandDollar wallets. However, only users who have undergone KYC (know your customer) verification can redeem their SandDollars with linked bank accounts.

Overall, the SandDollar wallet’s core financial infrastructure is being developed by The Central Bank of the Bahamas, however, each bank in the system is currently providing its own wallet to customers. Right now, it’s unclear if these wallets will be fully standardized, or will be somewhat customized to each bank’s specifications.

Jamaica

Advertisement for Jamaica’s JAM-DEX CBDC Wallet. Source: Bank of Jamaica.

Jamaica, like The Bahamas, also has a relatively advanced CBDC pilot program, spearheaded by the Bank of Jamaica (BOJ). Jamaica’s CBDC is called JAM-DEX, which stands for Jamaica Digital Exchange. Currently, only one institution, National Commercial Bank (NCB) offers a JAM-DEX wallet, which has been on the market for around a year.

NCB’s JAM-DEX wallet was created by a third-party digital payments and blockchain software development company, Lynk. In early 2023, the Bank of Jamaica stated that another bank, Jamaica National, would be the second approved wallet provider for the country’s CBDC. News reports also suggest that a third CDBC wallet provider will enter the market in the next few months, giving consumers additional wallet options when it comes to spending JAM-DEX.

The Status of CBDC Wallets In Other Countries

The status of CBDC wallets in countries that have not yet launched a CBDC varies widely. While data from the Atlantic Council states that 19 of the G20 countries are currently in an “advanced stage” of CBDC development, few countries have offered specifics on the wallets that CBDC users will utilize for payments.

Official logo and statement from the European Central Bank regarding their digital euro project. Source: Twitter/X (European Central Bank).

Many consider the European Central Bank’s (ECB’s) digital euro project to be one of the most advanced CBDC projects in the world today, so it’s little surprise that they’re one of the few banks to discuss some specifics about a potential digital euro wallet. Specifically, in June 2023, the ECB announced that its pilot digital euro wallet would likely allow users to store and spend up to $3,000 digital euros. The digital euro wallet could be used for both online and offline payments.

The ECB wants to strictly limit the amount of currency that can be stored in digital euro wallets to ensure financial stability by preventing major outflows from banks and any resulting shocks to the Eurozone’s monetary and financial system. However, many countries have voiced serious privacy concerns about the ECB’s CBDC program, and all 27 EU member states, and the European Parliament would need to agree to officially launch the digital euro, which some expect could be launched in 2027.

Official FedNow logo from the U.S. Federal Reserve. Source: Yahoo Finance.

In contrast, in the United States, little progress has been made on a retail CDBC in recent months, partially due to consumer privacy and human rights concerns. This means that we are unlikely to see a U.S. CDBC wallet being issued anytime soon. The U.S., however, is in the advanced stages of adopting a CBDC-like digital currency transfer system called Fednow, which would likely only be used for inter-bank transfers.

Other countries, including the Bank of England and the Bank of Japan, are also in the process of developing CBDCs, though it’s unclear when these will be launched and if wallets for digital pounds and digital yen will be issued by these countries’ respective central banks or a group of approved private banks.

In Conclusion: As More CBDCs Are Developed, The Number of CBDC Wallets Will Increase

CBDCs and CBDC wallets go hand-in-hand, as both are required for a CBDC to function correctly. However, since only a few countries have functioning CBDC wallets, there are really only a few examples of these wallets on the market today.

According to the Atlantic Council, only 11 countries have functioning CBDCs, with 8 of those utilizing the Eastern Caribbean Central Bank’s (ECCB’s) DCash CBDC wallet.

However, this could change soon, as 21 countries currently have active CDBC pilot programs, and overall, 130 countries (98% of global GDP) either have or are exploring a CBDC program. Therefore, we can expect many more CBDC programs (and CBDC wallets) to emerge in the coming years, each with its own risks, benefits, and unique features.

References:

- (Jan. 2022) China central bank launches digital yuan wallet apps for Android, iOS. Reuters.

- (Sep. 2023) eNaira. Central Bank of Nigeria.

- Newar, B. (Dec. 2021) Eastern Caribbean CBDC expands to another two territories. Cointelegraph.

- (Jul. 2023) India’s Retail Central Bank Digital Currency Project Makes Headway. FitchRatings.

- (May 2023) Press Release: Public Update on The Bahamas Digital Currency SandDollar. Central Bank of The Bahamas.

- (Aug. 2023) Third digital wallet provider expected to enter the market soon. Jamaica Gleaner.

- (Sep. 2023) Zero-knowledge Proof. Wikipedia.

- (Sep. 2023) China updates digital yuan wallet. Ledger Insights.

- (Aug. 2023) Bernstein, D. Could China’s Digital Yuan Challenge U.S. Dollar Dominance? Forbes.

- Ree, J. (Nov. 2021) Five Observations on Nigeria’s Central Bank Digital Currency. International Monetary Fund.

- (Sep. 2023) Organisation of Eastern Caribbean States. Wikipedia.

- Paul, M. (Jul. 2022) India still among countries with poor access to banking: Report. DownToEarth.

- (Sep. 2023) Lynk – Digital Payments. Lynk.

- Koutsokosta, E. (Jun. 2023) Brussels unveils plans for a digital euro promising complete privacy. Euronews.

- (Sep. 2023) FedNow Service. The Federal Reserve (FRBServices.org).

- (Sep. 2023) Central Bank Digital Currency Tracker. Atlantic Council.

RECENT POSTS

Get news, insights, and more

Sign up for the Supra newsletter for news, updates, industry insights, and more.

©2026 Supra | Entropy Foundation (Switzerland: CHE.383.364.961). All Rights Reserved