FedNow and Ripple: What You Need To Know

December 09, 2023 - 9 min read

Ripple Is Among The Nearly 60 Partners Approved To Integrate With FedNow

On June 29th, 2023, the Federal Reserve announced that it had approved 57 early adopter entities, including Ripple, as part of its FedNow pilot program. During the adoption process, Ripple and other financial services providers will undergo final trial runs on the service to ensure that it’s ready for widespread adoption.

This announcement marked the official integration of Ripple technology and XRP within the FedNow payment system, signaling a significant development in the use of blockchain technology and digital assets in the global financial system. In particular, it represents the Federal Reserve’s interest in incorporating private blockchain technology providers into its payment processing systems. It should also be noted that FedNow has relied on Ripple’s Interledger Protocol (ILP) technology to form the core of FedNow’s digital transaction infrastructure, meaning that this partnership is deeper than many might think.

The partnership between Ripple and FedNow has also dramatically increased interest in Ripple and its native XRP cryptocurrency, despite Ripple’s prolonged legal battle with the SEC in regards to accusations that Ripple Labs sold XRP as an unlicensed security.

What is FedNow?

FedNow marketing graphic. Source: The Federal Reserve.

FedNow, which launched in July 2023, is the Federal Reserve’s new instant payment service, which is mainly intended for bank-to-bank transfers and transfers between banks and other registered financial entities. Traditionally, the Federal Reserve has lagged significantly behind private payment services, and many consider FedNow as an attempt to remedy this discrepancy.

Is FedNow a CBDC?

While many have accused FedNow of being a subtle attempt to issue a CBDC (central bank digital currency) that could replace cash and traditional U.S. dollars, this is far from the truth.

According to the Federal Reserve:

“The FedNow Service is neither a form of currency nor a step toward eliminating any form of payment, including cash.

The Federal Reserve has made no decision on issuing a central bank digital currency (CBDC) and would only proceed with the issuance of a CBDC with an authorizing law.”

In addition, in his March 2023 testimony before the House Financial Services Committee, Federal Reserve chairman Jermome Powell assured legislators that the Fed would need direct congressional approval before issuing any kind of CBDC.

What is Ripple?

Ripple logo and graphic. Source: Ripple.com.

Ripple is a blockchain-enabled payment network utilizing the XRP cryptocurrency. Ripple, somewhat like FedNow, is generally intended for interbank transfers and transactions between major financial institutions, with a specific focus on cross-border transactions. In the context of the Ripple blockchain ecosystem, XRP cryptocurrency serves as a temporary settlement layer between two independent financial networks or between two different currencies. Ripple was created by a private company, Ripple Labs, in 2012.

Specifically, Ripple was designed to compete with the SWIFT (Society for Worldwide Interbank Financial Telecommunications) financial transfer network. While the average SWIFT transfer takes between 1-4 days (and sometimes longer), XRP transactions typically take between 3-5 seconds. In addition, transactions are quite affordable, with most transfers costing less than 1 cent.

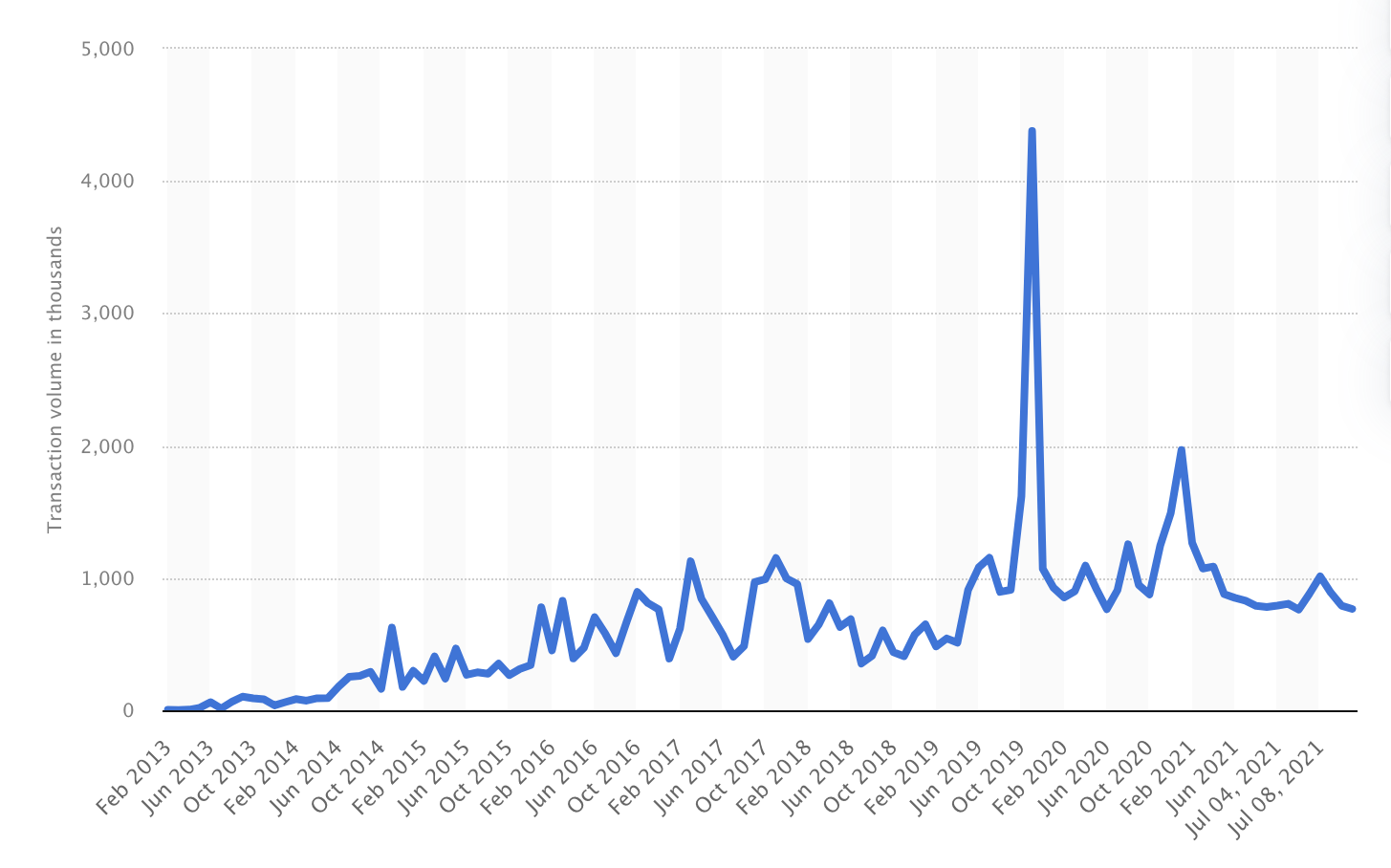

Ripple transactions per day, Feb. 2013 to Aug. 2023. Source: Statista.

The average XRP transaction takes about 3-5 seconds and costs less than 1 cent in fees.

As of late 2023, Ripple has partnered with a variety of well-known national and international banks and financial institutions, including Bank of America, Amazon Web Services, American Express, Banco Santander, and Standard Chartered Bank. In addition, Ripple also had a multi-year partnership with MoneyGram, but in 2021, MoneyGram decided to wind-down their partnership due to concerns over Ripple Labs’ lawsuit with the SEC.

While Ripple is one of best-known blockchains on the market today– and one of the few chains that has demonstrated real-world value outside the crypto ecosystem, many experts have significant concerns over the network’s level of centralization.

Much like many other blockchain networks, when the Ripple network started, Ripple Labs controlled the vast majority of the network’s nodes, as well as the vast majority of the chain’s native XRP currency, making the network extremely centralized. Many experts state that Ripple has taken an extremely slow road when it comes to decentralization, which is a core part of the SEC’s legal argument that XRP is a centralized security issued by Ripple Labs, not a decentralized commodity or currency.

However, Ripple has taken some important steps when it comes to decentralization. As of October 2022, Ripple announced that it had sold a significant amount of its XRP holdings (stating that it now owned less than 50% of all XRP), and, perhaps more importantly, it stated that it only operated four of the network’s approximately 130 validator nodes.

Despite these efforts, Ripple still remains incredibly centralized when compared to blockchains like Ethereum. For example, as of late 2022, the Ethereum Foundation, the most centralized entity associated with the Ethereum blockchain, stated that it only owned 0.3% of all ETH in circulation, and does not actively operate any validator nodes.

In addition to facilitating cross-border interbank and financial services transfers, Ripple is also developing a CBDC (central bank digital currency) platform, which would make it easier for central banks and governments to create and distribute CBDCs. This platform functions as an advanced and customized iteration of Ripple’s Private Ledger technology, helping facilitate major functions including minting, distribution, redemption, and token-burning.

The Technical Details of The FedNow’s Partnership With Ripple

Ripple’s technology partnership with FedNow goes much deeper than many might think. Ripple isn’t just a minor partner involved in testing the beta version of the FedNow transaction network– instead, Ripple’s underlying technology is actively being used as a core part of the FedNow system. Specifically, Ripple’s innovative Interledger Protocol (ILP) actually provides much of the technology infrastructure for FedNow’s transaction system. ILP is the core technology that enables Ripple, allowing the network to utilize the XRP cryptocurrency for secure, transparent, and near-instantaneous cross-border transactions.

What Other Entities Are Part of the FedNow Pilot Program?

According to a June 2023 press release from the Federal Reserve, some of the best known entities (other than Ripple) that are currently partnered with the FedNow program include BNY Mellon, JPMorgan Chase, U.S. Bank, and Wells Fargo Bank.

What Does This Partnership Mean For The Future of Blockchain?

Overall, as previously mentioned, the Fed’s partnership with Ripple shows us their increasing interest in public-private partnerships within the blockchain technology space. This could be a positive indicator that the Fed wants to support innovative technologies and create a more efficient, equitable financial system. Alternatively, it could indicate that the Federal Reserve simply wants more insight and influence over the development of blockchain technology in order to preserve its own influence over the U.S. (and global) monetary and financial system.

This partnership could be one of many to come, and, it’s unlikely, but possible, that the Fed could partner with more organizations and protocols in the blockchain community, such as Layer-1 and Layer-2 blockchains and DeFi protocols like MakerDAO, creating the potential for a greater degree of monetary decentralization.

FedNow’s Partnership With Ripple And Volante: Could It Boost Ripple’s Popularity?

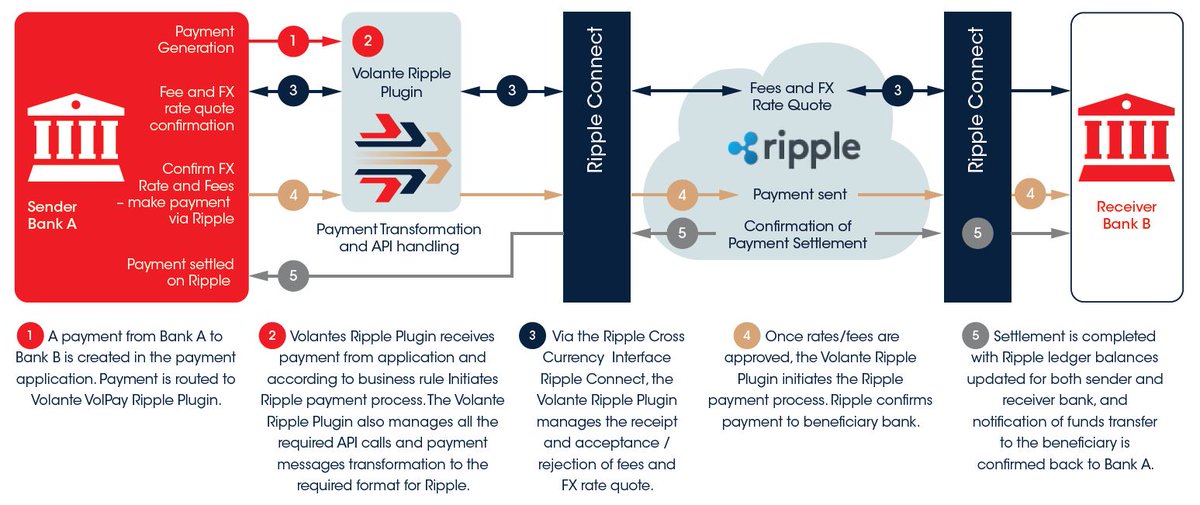

Flowchart describing Volante and Ripple’s interbank transfer system. Source: Twitter/X: BankXRP.

While Ripple’s partnership with FedNow runs deep, there’s actually a third party that is also involved in the partnership– the software company Volante. Volante is a major client and partner of FedNow, and has also significantly contributed to the development of FedNow’s technological infrastructure. Some believe that this partnership is further good news for the Ripple ecosystem, and could give an additional boost to XRP prices, particularly if Ripple wins its lawsuit with the SEC.

FedNow vs. Ripple: Are They Competitors?

While it’s true that FedNow and Ripple have a strong partnership, some see the two entities as competitors, rather than partners, and this concept may have some degree of truth. While Ripple may be integrated into the FedNow network, both FedNow and Ripple are fast, low-cost, interbank financial transfer networks, and they may be competing for market share.

In a contest between the two, FedNow has certain advantages, as it is backed by what many consider the most influential financial institution in the world, giving it significant power when it comes to shaping regulations that could benefit the growth of the FedNow network.

However, Ripple has its own set of advantages over FedNow. For one, as a private, semi-decentralized enterprise, Ripple may be able to move much faster, creating better and more innovative financial solutions than the Fed, which could be tied down by the same regulations that it hopes to influence. Plus, Ripple might be trusted more than the Federal Reserve, an institution that some believe has misused its power in a variety of ways. In addition, FedNow’s focus is mainly on U.S. interbank and financial services transfer, while Ripple has partnerships all around the world, which could give it an edge when it comes to overall adoption.

Finally, Ripple may be seen as a more private option than FedNow, as using FedNow directly gives a government organization both power and detailed information about financial transactions, information that some institutions would rather remain somewhat more private.

Could Ripple’s FedNow Partnership Impact Its Lawsuit With The SEC?

In addition to furthering Ripple’s profile, Ripple’s FedNow partnership could potentially influence the result of its lawsuit with the SEC. While the Federal Reserve is not a judicial enforcement agency and has no direct control or authority over the SEC, it’s still a very powerful organization– meaning that it could exercise some degree of subtle influence over the intensity of the SEC’s legal battle against Ripple.

Plus, the Federal Reserve is highly unlikely to initiate a major partnership with an organization that it believes is likely to be shut down (or severely impacted) by government judicial action. This means that insiders at the Fed might know something the public doesn’t know about the inside details of Ripple’s lawsuit with the SEC. Therefore, theoretically, it could have evidence or information to suggest that Ripple will win, rather than lose, its lawsuit.

In Conclusion: Ripple’s Partnership With FedNow Bodes Well For Ripple, But The Final Outcome Is Still Unclear

FedNow’s close partnership with Ripple has likely helped the Federal Reserve develop its financial transfer technology significantly faster, with a higher degree of interoperability and security than it would have been able to create on its own. This is perhaps the biggest incentive for the Fed to continue its partnership with Ripple, despite the controversy surrounding Ripple’s legal battle with the SEC. For Ripple, the FedNow partnership is a major boon and has likely helped sustain the price of XRP during challenging market conditions. If the partnership continues to expand, and Ripple emerges victorious from its lawsuit, Ripple could gain increasing influence as a major player in the global financial system.

References:

- (Jun. 2023) Organizations Certified as Ready for the FedNow® Service. The Federal Reserve.

- Dzhondzhorov, D. (Sep. 2023) Ripple v. SEC Lawsuit Important Update: Sep 26th. CryptoPotato.

- (Sep. 2023) Is the FedNow Service replacing cash? Is it a central bank digital currency? The Board of Governors of the Federal Reserve System.

- Frankenfeld, J. (Jul. 2023) Ripple Definition. Investopedia.

- Smith, M. SWIFT Transfers explained (Everything you need to know!) Key Currency.

- Duggan, W. (Jul. 2023) Ripple (XRP) Definition. US News and World Report.

- (Jul. 2023) Biggest Ripple Partnerships – How XRP Revolutionized the Blockchain Industry. Coindoo.

- (Mar. 2021) Blockchain firm Ripple to end partnership with MoneyGram. Reuters.

- Smith, A. (Oct. 2022) Ripple’s now owns less than 50% of XRP crypto and operates just 4 of the 130 validator nodes. The Coin Republic.

- (Sep. 2022) Sephton, C. Revealed: How Much ETH is Owned By the Ethereum Foundation. CoinMarketCap.

- (Jul. 2023) Ripple Partner Volante To Take FedNow Cross-Border After Regulation, XRP To $1? CoinGape.

- Ngetich, D. (Feb. 2022) US Fed To Launch FedNow In July, Countering Ripple? NewsBTC.

- (Jul. 2023) What Is the Fed’s Relationship to Ripple’s Victory? Altcoinbuzz.

RECENT POSTS

뉴스, 인사이트 및 더 많은 정보를 받으세요.

뉴스, 업데이트, 업계 인사이트 등 다양한 정보를 받으시려면 Supra 뉴스레터에 가입하세요.

©2026 Supra | Entropy Foundation (스위스: CHE.383.364.961). 판권 소유