Crypto and Commodities: What You Need To Know

December 11, 2023 - 13 min read

Some Cryptos Are Classified As Commodities, While Others May Be Classified As Securities

Some cryptocurrencies are classified as commodities in certain countries, including the United States. For example, in the U.S., Bitcoin and Ethereum are currently regulated by the U.S. CFTC (Commodities Futures Trading Commission) as commodities, like gold and silver. In contrast, a “crypto commodity” is a different type of asset than a traditional cryptocurrency. A crypto commodity is generally considered a token representing a real-world or virtual commodity, asset, utility, or contract. However, it’s important to note that not all popular cryptocurrencies are commodities.

For example, some cryptocurrencies have been classified as securities, and the legal classification of some cryptocurrencies is currently unclear. This can often happen in cases where laws have not yet been drafted or in situations where there is ongoing legal action.

One famous example is the ongoing litigation between the U.S. Securities and Exchange Commission (SEC) and Ripple Labs, which created the popular Ripple (XRP) cryptocurrency. The SEC has consistently argued that Ripple Labs has violated U.S. federal laws by selling unlicensed securities. While Ripple did achieve a partial legal victory when, in July 2023, a judge ruled that XRP is not a security, the judge did not classify XRP as a commodity or currency, leaving the cryptocurrency’s legal status unclear.

However, in September 2023, the SEC formally appealed the judge’s ruling, and the organization appears to be putting significant resources into attempting to win the case. A win for the SEC could lead to more cryptos being classified as securities rather than commodities or currencies. This, in turn, could lead to a significant damper on the crypto market, especially in the United States.

Why Bitcoin and Ethereum are Classified as Commodities

Before discussing why Bitcoin and Ethereum are currently regulated as commodities by the CFTC, let’s first take a quick look at the legal definition of a commodity and what makes it different than a security (or a currency, for that matter).

Traditionally, assets like gold, silver, oil, or wheat are considered commodities. These assets all have a few things in common, including:

- They are not formed, controlled, or issued by one or a few known entities. Instead, they are created or harvested by diverse individuals and groups without a single goal, identity, or specific location, whether physical or digital.

- No single entity gains financial advantages or suffers disadvantages from the price activity of the asset. Instead, many entities may gain financial advantage or suffer financial disadvantage due to the asset’s price activity, depending on their specific actions.

- They are fully fungible; for example, one Bitcoin or one bushel of corn (assuming the corn is of a standard type and quality), which we can identify as a unit, is, in theory, of equal value to all other units. For instance, no “class A type” of Bitcoin can provide more voting rights and corporate responsibilities than a “class B type,” as we can see with stocks and, to some extent, bonds.

Howey Test diagram. Source: SEC/Crypto News.

In contrast, securities, which, in the United States, are currently defined by the Howey Test, have a different set of core characteristics, including:

- A security is defined as a type of “investment contract.”

- An investment contract occurs when there is “investment of money in a common enterprise with a reasonable expectation of profits to be derived from the efforts of others.”

- In addition, the investor in a security “is led to expect profits solely from the efforts of the promoter or a third party.

Therefore, for an asset or contract to qualify as a security, there must be:

- “An investment of money

- In a common enterprise

- With the expectation of profit

- To be derived from the efforts of others.”

For example, Bitcoin is generated by thousands of miners distributed worldwide. There is no centralized company or organization behind Bitcoin. Therefore, it is not a “common enterprise.” The price of Bitcoin is not primarily determined by the efforts of one or a few entities and is instead determined by market supply or demand. As previously mentioned, Bitcoin is fungible, so each is precisely the same as every other.

Ethereum, while now a proof-of-stake network, has many of the same qualities as Bitcoin, including hundreds of thousands of node operators distributed worldwide. While there is an Ethereum Foundation that helps advocate for Ethereum developers, it currently owns less than 0.3% of all ETH in circulation, meaning that it has almost no influence over the network, and, in general, the efforts of the Ethereum Foundation do not have a discernable impact on the price of ETH.

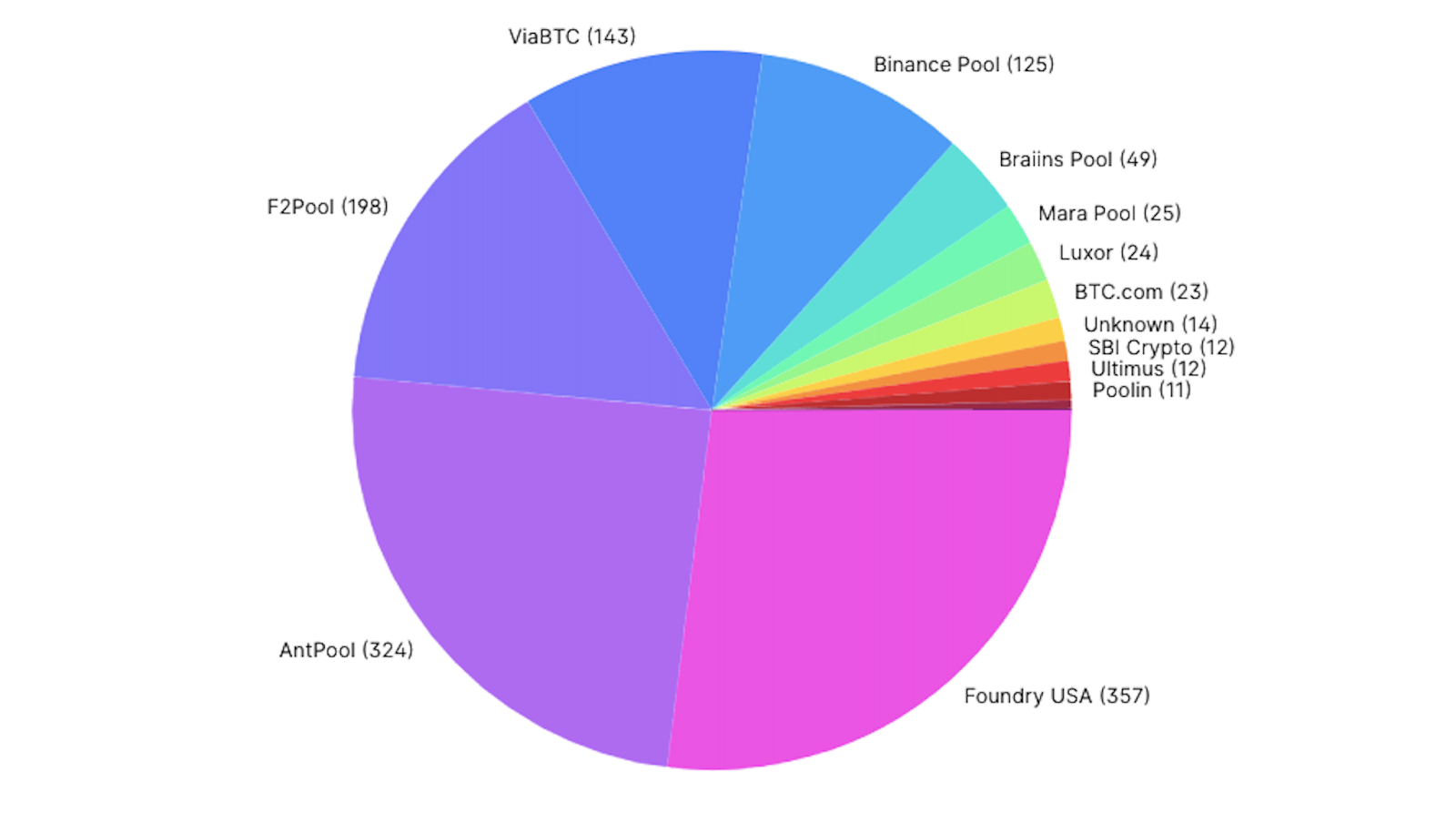

Bitcoin hashrate pie chart, showing AntPool and Foundry USA as representing more than 51% of Bitcoin’s total hashate (Jan. 2023). Source: CryptoSlate.

Of course, there are some points of centralization when it comes to Bitcoin and ETH, particularly when it comes to mining pools. For example, as of early 2023, only two mining pools were responsible for around 50% of Bitcoin’s hashrate. This means there is a very small possibility that these pools could collude to attack the Bitcoin network. However, it should be noted that these pools themselves are not monolithic; instead, they consist of thousands of individual miners who have pooled their resources. Therefore, if it appeared these networks were manipulating the Bitcoin network, it’s highly likely that many miners would leave these pools, significantly reducing their hashrate and, therefore, making it impossible for them to conduct a 51% attack successfully.

How The CFTC Came To Classify Bitcoin and Ethereum As Commodities

According to former CFTC Chairman Christoper Giancarlo, the CFTC took early and proactive action to classify Bitcoin as a commodity. In December 2014, then CFTC Chairman Timothy Massad testified before the U.S. Congress that Bitcoin was a commodity and should, therefore, be under CFTC jurisdiction.

Giancarlo said:

“In 2015, again, with my support the CFTC in a case called the Coinflip case, declared Bitcoin, as a matter of law, to be a commodity and subject to the CFTC. And then under my leadership as chairman of the agency in 2015, we greenlighted the first U.S regulated market for Bitcoin Futures under the exclusive jurisdiction of the CFTC.”

This action later led to CFTC rules that would also put Ethereum under the organization’s regulatory jurisdiction.

Examples of “Crypto Commodities” (Rather Than Cryptos Classified as Commodities)

While they may sound like the same thing, a “crypto commodity” and a crypto classified as a commodity are two distinct types of assets. While a cryptocurrency only has to demonstrate a high level of decentralization to be (potentially) legally classified as a commodity, a crypto commodity is a cryptocurrency or token “representing a commodity, utility, asset, or contract in the real or virtual world.”

This means that assets like gold-backed stablecoins like Paxos Gold (PAXG), Tether Gold (XAUT), and Gold Coin (GLC) could potentially be classified as crypto commodities, as they are backed by, and can generally be exchanged for real-world gold. In addition, it’s also possible that stablecoins like Tether (USDT) or and USD Coin (USDC) could be classified as crypto commodities, as they represent a contract in which the stablecoin can be exchanged for real U.S. dollars on a 1:1 basis.

Other types of asset-backed tokens, such as tokens that are backed by real estate, oil, or other assets, and even tokens that are backed by other cryptocurrencies, such as wrapped Bitcoin (WBTC), which can be exchanged on a 1:1 basis for BTC, could also classify as crypto commodities.

Cryptocurrencies as Commodities and Securities Outside The United States

While most of this article has discussed the legal status of cryptocurrency inside the U.S., it might also be useful to look at crypto’s legal classification in other countries. So far, the U.S. has been the only country to regulate certain cryptos as commodities. In contrast, in the U.K., they are classified as “cryptoassets,” a new type of asset that is neither a commodity, a security, or a currency.

By creating a new legal framework around crypto, the U.K. government hopes to enjoy the innovation and economic growth generated by the crypto and blockchain economy while preventing the darker side of the industry– including helping stop crypto-related crime, scams, Ponzi schemes, especially when these issues could hurt the broader economy.

Which Cryptocurrencies Are The Most Likely To Be Classified As Securities Instead Of Commodities?

In June 2023, the SEC announced that it would consider 68 cryptocurrencies as securities, representing a market cap of over $100 billion. But what traits most likely impact the SEC’s decision to label a crypto as a security?

Generally, any cryptocurrencies that pass the Howey Test are more likely to be classified as securities rather than commodities. As discussed earlier in this article, the Howey Test defines a security as an ‘investment of money in a common enterprise, with the expectation of profit to be derived from the efforts of others.’ Therefore, projects with the following characteristics are the most likely to be classified as securities:

- Price Influence: Projects where the founding team or founding company exerts strong control over the blockchain protocol or network. In these situations, the founding team likely significantly influences the price of the network or protocol’s native asset (in this case, profit is derived from the efforts of others).

- Token Distribution: Projects in which the founding team, early VC investors, or individuals closely associated with the founders own and/or control a large percentage of the protocol or blockchain’s native cryptocurrency.

- Validator/Note Centralization: Projects with few or no independent validators/nodes or projects in which a large percentage of the validators are controlled by the founding company or team or closely related individuals are entities.

- Public Statements: Projects that have made public statements indicating that improvements or developments to the project executed by the founders will impact the token price.

- Availability To U.S. Investors: Projects in which the native cryptocurrency or token is sold on one or more popular and easily accessible centralized crypto exchanges (i.e., Coinbase, Binance U.S., Kraken, etc.)

- Overall Decentralization Level: Projects controlled by companies are more likely to be classified as securities, while projects controlled by DAOs, provided that the DAOs are sufficiently decentralized, may not be as likely to be classified as such.

Further list from SEC lawsuit of other 7 cryptos involved in the ligitation and the SEC’s arguments as to why they are securities.

Why Can’t Cryptocurrencies Simply Be Classified as Currencies?

It seems like a simple question: if cryptocurrencies are intended to replace traditional currency, why can’t they simply be classified as currencies rather than commodities or securities? Well, the answer is complex, but the core reason is that, in most countries, there isn’t a functional legal framework to classify any assets as currencies that are not issued by a country’s central bank.

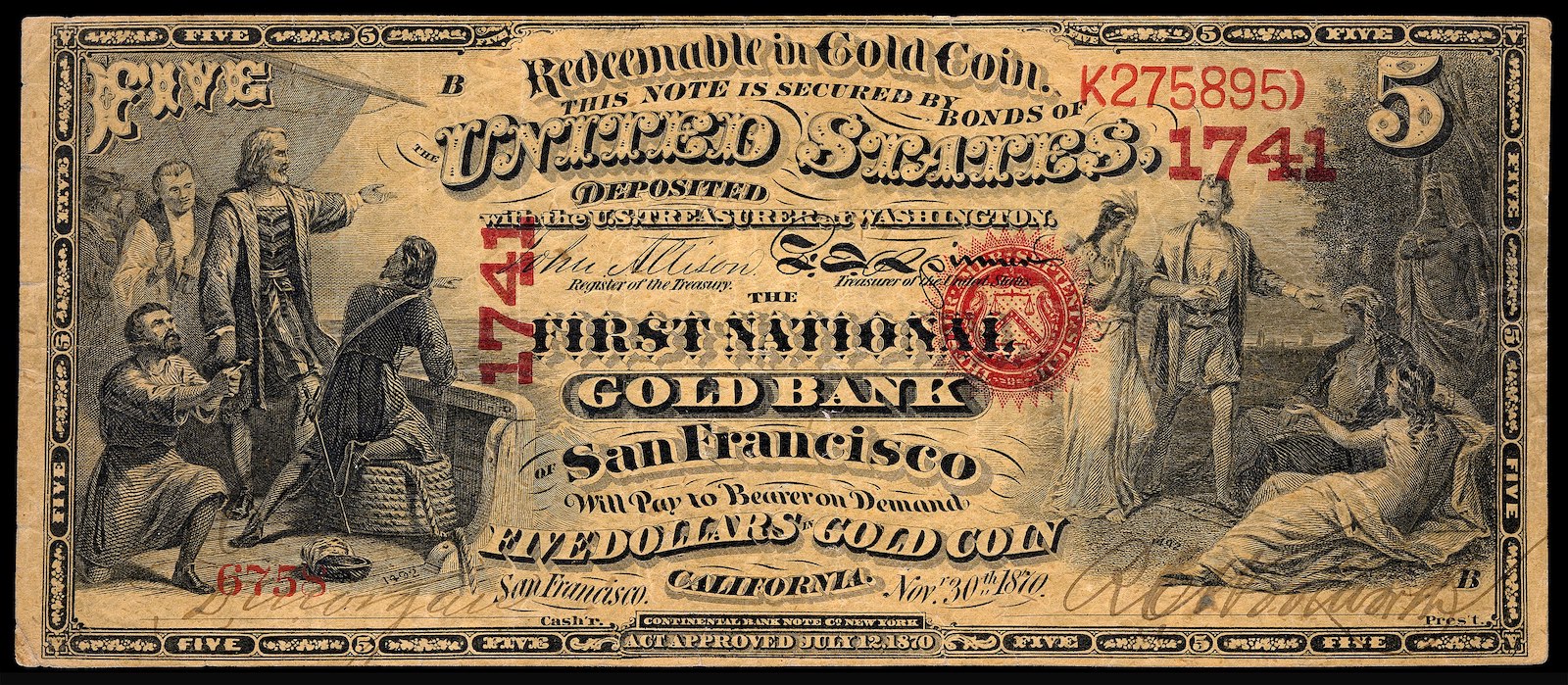

However, this doesn’t mean that there’s never been a legal framework– for example, in the 19th century, a variety of private U.S. banks actually offered their own currencies, some backed by gold or silver, others simply backed by trust in the bank itself. While this gave consumers many choices regarding currencies, many of these banks failed, making their currencies worthless and leaving many bereft of their life savings. These issues eventually led to more centralization and promotion of the U.S. dollar, and eventually, banks were prohibited from issuing private currencies in the United States.

1870s $5 note issued by the First National Gold Bank of San Francisco during America’s free banking era. Source: CoinDesk.

Despite this, there have been other examples in which private currencies have had a significantly more positive impact on a country’s financial, economic, and monetary systems. For example, “free banking,” a system in which private banks were allowed to issue their own currencies with very little regulation, existed in Scotland between 1716 and 1845, resulting in an exceptionally stable and effective monetary system.

More than 60 countries have experimented with free banking systems over the last one thousand years. While results have been mixed, it’s clear that, if implemented correctly, such a system might produce superior results than our current system of fiat central banking.

However, much of our political, economic, and social systems currently revolve around the influence of the Federal Reserve and other central banks, so it is highly unlikely that free banking systems will be implemented anytime soon, and, as a result, crypto is unlikely to be regulated or defined as a currency in the near future.

Are NFTs Commodities Or Securities?

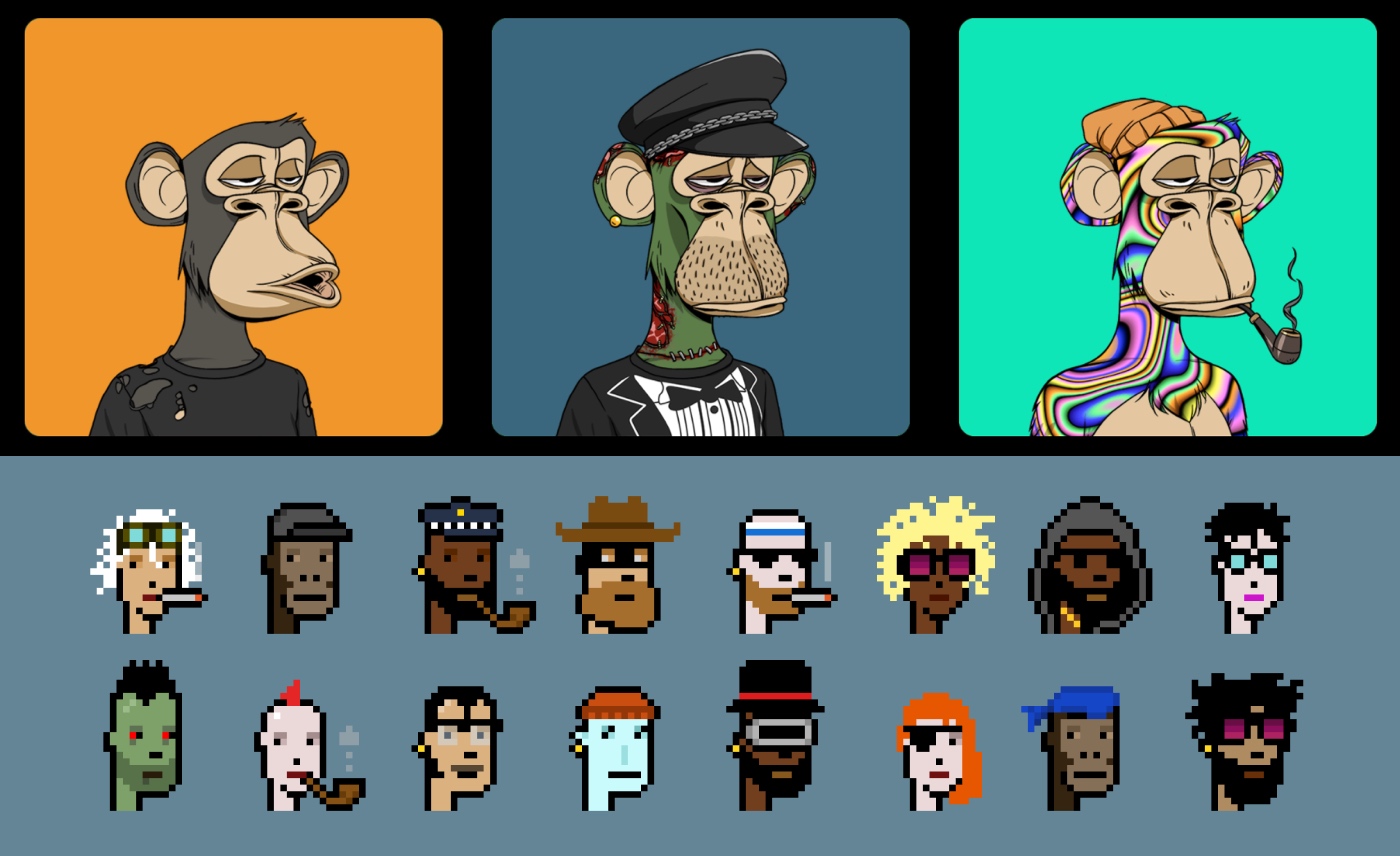

Two of the most popular NFT collections: Bored Ape Yacht Club and CryptoPunks: Source: The New Stack.

While the legal status of cryptocurrencies, especially smaller cap assets, is in limbo– in most countries, the status and classification of NFTs is even more unclear. An NFT could be a commodity, a security, or neither. “Simple” NFTs– such as PFP art NFTs like the Bored Ape Yacht Club or CryptoPunks, are likely to be neither a commodity nor a security.

However, asset-backed NFTs, like asset-backed cryptocurrencies, might be classified as securities or commodities. If the NFT is backed by commodities or assets like real estate or collectibles, which do not typically rise in price due to the efforts of others (and therefore do not pass the Howey test), these NFTs would likely be classified as commodities. In contrast, NFTs representing some type of share or stock (or even a bond) in an actively managed business might be classified as securities.

However, there are many complexities and details to consider here. For instance, an NFT representing the ownership of a house might be a commodity– but an NFT representing ownership in a real estate development company building an apartment complex is more likely to be classified as a security.

Royalty-sharing NFTs, which provide a share of the sales price to the original creator each time an NFT is sold or traded, also exist in a potential gray area regarding legal classification. For instance, if a rapper issues a profit-sharing NFT that will provide users a particular share of the profits from their concert tour, that might be a security, as the financial gains experienced by the NFT holders would be considered the “efforts of a single enterprise,” and might therefore pass the Howey Test. In contrast, a royalty-sharing NFT issued by the same rapper that simply gives the rapper a portion of the sales proceeds each time the NFT is resold might be classified as a commodity (or might not be classified at all).

Blockchain Technology and the Traditional Commodities Industry

Commodities trading at the Chicago Mercantile Exchange (CME), the world’s largest commodities trading exchange. Source: Enjoy Illinois.

Most of this article discusses the classification of cryptocurrencies as commodities or securities. Blockchain technology, which provides the technical infrastructure for all cryptocurrencies, might also have a powerful impact on traditional commodities markets.

According to a recent report by S&P Global, blockchain technology, when applied to commodities markets, has a variety of potential benefits. These include cutting trading and transaction costs, enabling better wholesale peer-to-peer trading without the extensive use of third parties, helping enable more efficient derivatives trading, and potentially cutting down on fraud, particularly trade-based money laundering.

Currently, pilot projects are in process worldwide, with Singapore being one of the most prominent global hubs for blockchain commodities projects.

In Conclusion: Cryptocurrency And Commodities Have a Complex Relationship

Depending on where you are, who you talk to, and which cryptocurrency you’re discussing, cryptocurrencies may be classified as commodities, securities, or neither. The CFTC’s (Commodities Futures Trading Commission’s) classification of Bitcoin and ETH as commodities has enabled new and traditional institutions to trade crypto futures on the world’s largest government-regulated commodities exchange.

This has greatly boosted the crypto market, adding significant liquidity to BTC and ETH while helping crypto and blockchain technology become significantly more commonplace (and mainstream) in the finance industry.

However, the SEC’s legal battles against Binance, Ripple, and other entities are already putting a significant damper on the crypto market– and while it looks like Ripple may win its’ case, a loss could seriously impact crypto trading in the United States. It could even force exchanges like Coinbase to delist dozens, if not hundreds, of popular cryptocurrencies, which might devastate the broader crypto industry.

It should be noted, however, that the relationship between crypto and commodities goes further than just government asset classifications. Specifically, new “Crypto commodities,” cryptocurrencies or tokens representing ownership shares in real-life commodities (like gold-backed cryptos) or even other cryptocurrencies (i.e., wrapped BTC), are becoming increasingly popular.

Finally, blockchain technology, though not necessarily cryptocurrency itself, is also expected to have an increasing impact on traditional commodities trading by reducing transaction fees, increasing transaction speeds, improving security, and preventing fraud.

As governments continue various cryptocurrency classification schemes, crypto commodities continue to evolve, and traditional commodities trading engages further with blockchain technology, we expect commodities to have an increasing impact on the crypto and blockchain industry in the near future.

References:

- Torpey, K. (Jul. 2023) What Does The ‘XRP Not A Security’ Ruling Mean For Other Cryptocurrencies? Investopedia.

- Dzhondzhorov, D. (Sep. 2023) Important Ripple (XRP) v. SEC Lawsuit Update Sep 29th. CryptoPotato.

- Reiff, N. (Jul. 2023) Howey Test Definition: What It Means and Implications for Cryptocurrency. Investopedia.

- Morales, J. (May 2023) Ethereum (ETH) Faces Potential Price Dip Amid Foundation Selloff. BeInCrypto.

- Adeniyi, O. (Feb. 2023) Data Shows 50% Of Bitcoin Hashrate Controlled By Two Mining Pools. Bitcoinist.

- When is cryptocurrency a commodity? Talks On Law.

- (Jul. 2023) Top 6 Gold Backed Cryptocurrency For 2023 [Updated List]. Software Testing Help.

- What are Asset-Backed Cryptocurrencies? Solulab.

- (Jun. 2023) Factsheet: cryptoassets technical. Gov.uk.

- Coghlan, J. (Jun. 2023) SEC lawsuits: 68 cryptocurrencies are now seen as securities by the SEC. Cointelegraph.

- (Oct. 2022) Free banking. Wikipedia.

- 2018: Blockchain for Commodities: Trading Opportunities in a Digital Age. S&P Global.

RECENT POSTS

뉴스, 인사이트 및 더 많은 정보를 받으세요.

뉴스, 업데이트, 업계 인사이트 등 다양한 정보를 받으시려면 Supra 뉴스레터에 가입하세요.

©2026 Supra | Entropy Foundation (스위스: CHE.383.364.961). 판권 소유