CBDC Mining: Can CBDCs Be Mined?

November 15, 2023 - 8 min read

CBDC Mining: A Move Toward A Semi-Decentralized CBDC?

Currently, no CBDCs or central bank digital currencies can be mined. However, creating a proof-of-work, mineable CBDC could be an attractive, yet highly controversial possibility and could lead to the creation of a semi-decentralized CBDC. CBDCs, or central bank digital currencies, are centralized cryptocurrencies that government central banks issue. Typically, these currencies are backed 1:1 by the same fiat currency issued by the central bank. They are usually issued on specialized private government blockchains and can be stored in government-issued CBDC wallets.

CBDCs have come under harsh criticism by many crypto advocates, as they can potentially allow governments and central banks to closely track people’s financial transactions, possibly undermining an individual’s right to privacy. In addition, some worry that governments might restrict people’s transactions– and even assign them social credit scores based on arbitrary metrics, which could gravely impact civil rights. In contrast, CBDC advocates see CBDCs as facilitating various government transactions, such as welfare payments, increasing transparency, and reducing government fraud.

While CBDCs may have a bad reputation among blockchain advocates, there may be ways to make CBDCs better, safer, and more transparent– and CBDC mining (or staking) could be one of them.

How Crypto Mining Currently Works

To see how CBDC mining might work, let’s first look at the most popular proof-of-work cryptocurrency, Bitcoin. Currently, new Bitcoins are mined by computers that perform an increasingly complex set of randomized mathematical calculations to earn the right to “mine” the next block, validating a set of transactions on the Bitcoin blockchain. By mining the block, they receive a certain amount of Bitcoin as a block reward. While mining is certainly an effective way to promote blockchain decentralization, and when a proof-of-work network reaches a certain size, it becomes pretty secure, as 51% of attacks and other network manipulations become extremely difficult– and extremely expensive.

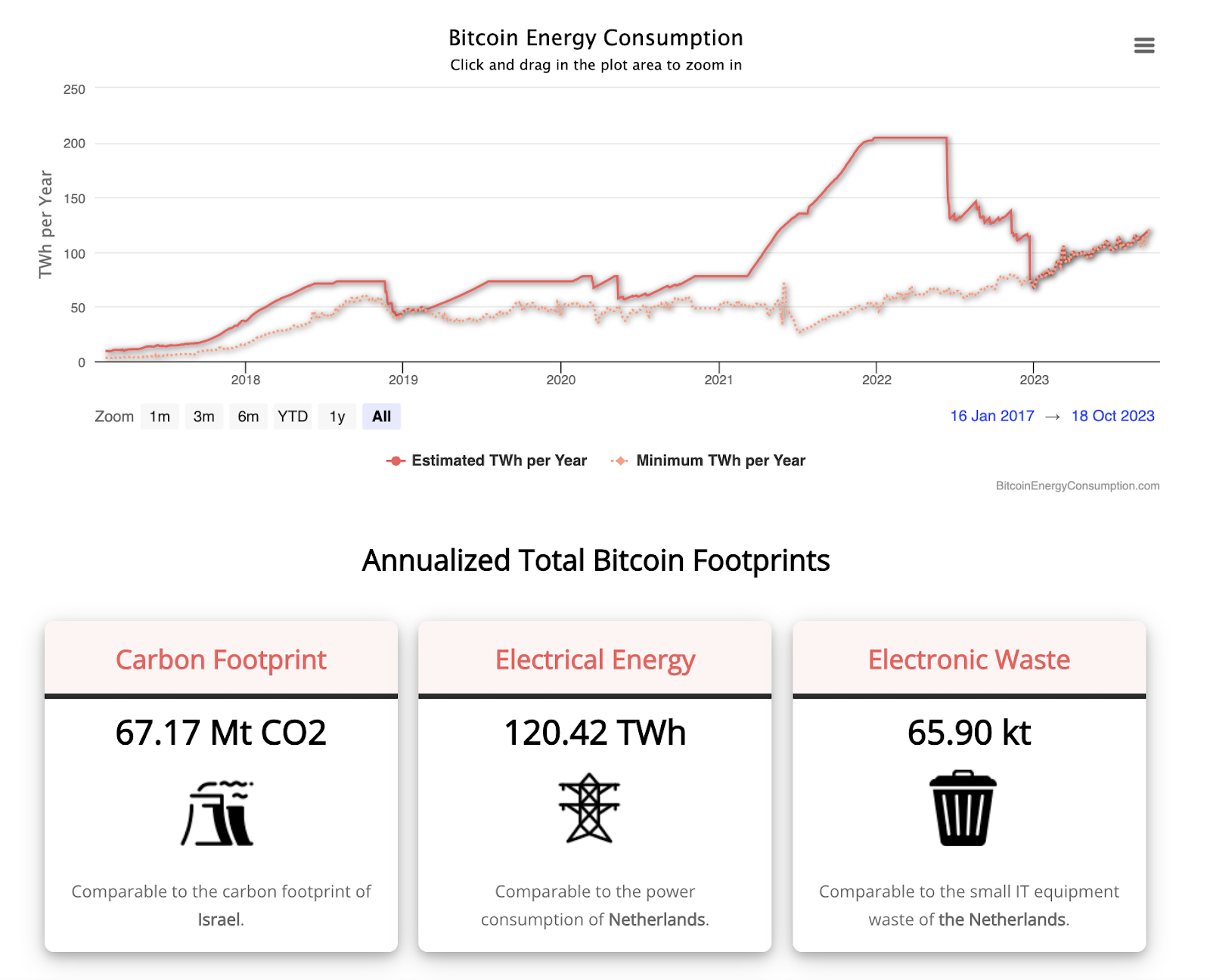

Bitcoin energy consumption and carbon footprint, 2017- 2023. Source: Digiconomist.

However, for blockchains like Bitcoin, mining can be extremely energy intensive, as mining at scale requires specialized computer processors called ASICs (application-specific integrated circuits), which consume a significant amount of electricity. Most professional Bitcoin mining operations have hundreds if not thousands (or tens of thousands) of these ASICs, all of which must be powered 24/7 and perpetually cooled to continue mining. In fact, according to research from the Rocky Mountain Institute, Bitcoin mining utilizes 127 terawatt-hours (TWh) of electricity per year. This exceeds the entire electrical consumption of many countries, including Norway. In the United States alone, crypto mining (mainly Bitcoin mining) emits an estimated 25 to 50 million tons of carbon dioxide annually.

How Fiat Currency Is Currently “Created”

Now that we know how crypto mining works, how would it work for a central bank digital currency? Well, instituting a CBDC mining program would require a significant change to the legal, monetary, and economic framework of the country issuing the CBDC. Therefore, it would likely have to be approved at the highest political levels.

Crypto mining creates new currency– and so would CBDC mining. To understand this issue better, let’s look at how countries “create” fiat currency. While “create” may not be the most accurate term, it’s probably the most accurate term we can use without diving deep into the weeds of monetary policy and macroeconomics. Generally, national central banks create new currency by issuing government bonds, which are sold to the public and can be easily purchased by retail and institutional investors.

After issuing the bond, the bond sale proceeds are credited to the country’s treasury, which can then spend the money. This type of monetary creation allows countries to spend as much as they want by issuing new bonds, which can be extremely problematic in the long term, as it can lead to an increase in the money supply, leading to inflation. This makes common goods and services more expensive and reduces the purchasing power of average consumers, mainly since wages generally do not rise as fast as inflation does.

CBDC Mining and Decentralized CBDCs: Potential Economic Models

To allow a CBDC to be mined would likely transfer some degree of power from the central bank to the miners, creating a more decentralized system, though semi-decentralized structures are undoubtedly possible.

The most radical proposal would involve a country entirely switching from a traditional fiat currency to a CBDC and allowing for the creation of a considerably more decentralized banking system. This possibility would allow a decentralized network of miners to determine how much of a currency would be issued. At the same time, this network could have the power to order the country’s treasury to issue digital CBDC bonds, and for every dollar of bond issued, a new CBDC would be able to be mined.

Instead of a monolithic blockchain, each bond could have its own modular blockchain, side chain, or parachain for each bond issuance, and, much like Bitcoin, miners would receive transaction fees for creating new coins. Much like Bitcoin, the mining process could become harder and harder as more of the coins are mined, and, in addition, the amount of currency that could be mined could be set at a hard cap in order to prevent inflation.

While this system would be interesting and relatively decentralized, it may not have the correct economic incentives to promote a better monetary system, and, since miners would make more money the more currency is issued, it could actually increase inflation, as miners would have a strong incentive to keep mining to earn more transaction fees.

A less decentralized proposal would have the country’s treasury and central bank still retaining the power to issue as many bonds as they want without a hard cap. Still, miners could earn transaction fees by mining more of the currency up to the specific cap of the latest bond issuance. However, it’s unclear whether having these miners would benefit the country’s monetary policy in any way.

CBDC Mining vs. CBDC Staking

While CBDC mining is a popular topic, in practice, a decentralized or semi-decentralized CBDC would likely operate as a proof-of-stake (PoS) currency rather than a proof-of-work one. This is because of the previously mentioned environmental impact of proof-of-work cryptocurrencies and the fact that, despite early concerns, proof-of-stake appears to be relatively secure (even when compared to proof-of-work systems), as evidenced by the relatively high security level of chains like Ethereum and Solana.

MakerDAO as a Model for a Semi-Decentralized CBDC

Despite the issues with the decentralized CBDC models we discussed earlier in the article, one stablecoin could serve as a potential model for a decentralized CBDC that could utilize mining or staking as a consensus mechanism.

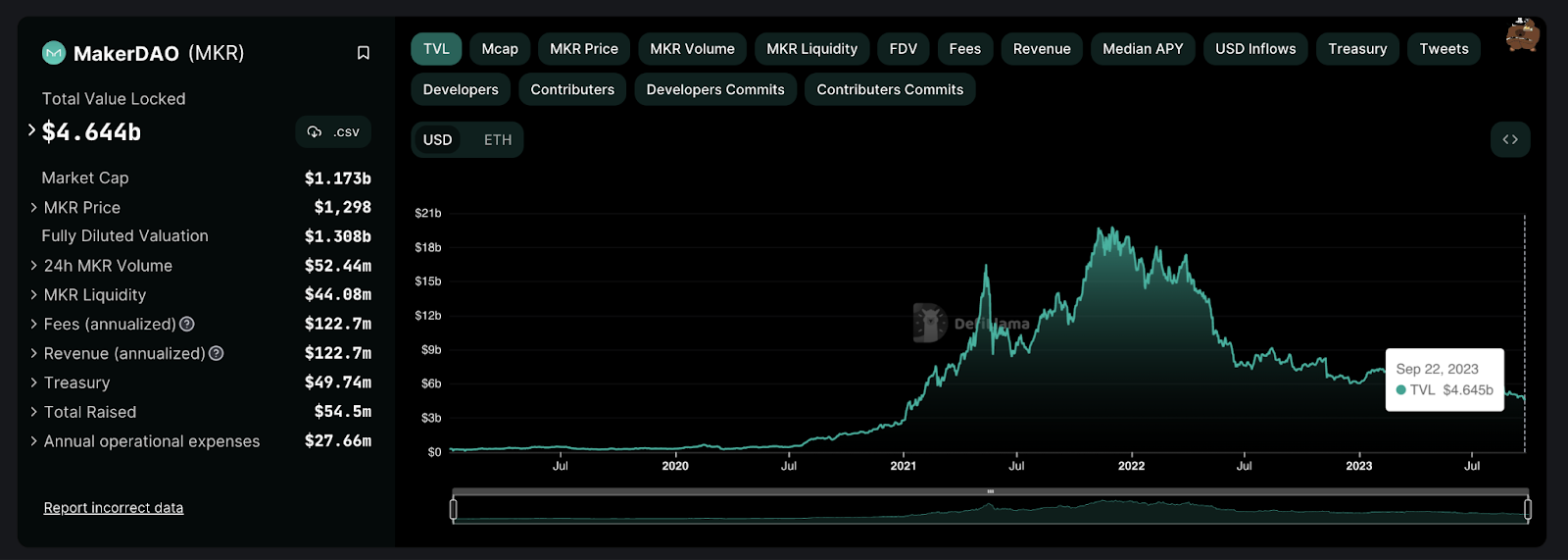

MakerDAO, a popular blockchain ecosystem and “decentral bank,” which issues the popular stablecoin, DAI, has weathered multiple crypto downturns and is perhaps the only genuinely stable decentralized stablecoin on the market today. To mint the DAI stablecoin, individuals must lock up a specific amount of ETH or other cryptocurrencies in a smart contract. It’s essential to note that DAI is an overcollateralized stablecoin; for example, users generally must lock up 150% of the value in ETH of the DAI they want to mint before getting authorization to mint the coins.

MakerDAO ecosystem and TVL (total value locked) data, Sep. 2023. Source: DefiLlama.

For instance, if you wanted to mint $10,000 of DAI, you’d have to lock up around $15,000 in ETH in a Maker smart contract. Users can later get their ETH back (at its current market price) by exchanging it for the DAI they minted previously. Users are incentivized to mint DAI since they can lend it out on various crypto lending protocols to earn yield, and they can always get their ETH back later. This over-collateralization generally helps ensure that DAI retains its value even when the crypto market takes turns for the worse.

But how does this relate to CBDC mining and staking? A decentralized system could be created where users can exchange assets with real value, such as gold, stocks, bonds, or real estate, for a CBDC coin (backed by a central government). Much like in the MakerDAO model, they could then lend these coins out for extra yield while still being able to later exchange their assets (at their current market value) for the amount of CBDCs they initially minted. Transferring the CBDC from wallet to wallet would carry transaction fees, some of which would go to stakers and some to purchase more real-world assets to add to the CBDC treasury.

To combat inflation and create a potentially inflation-resistant CBDC, some of these real-world assets could be sold to buy back CBDCs at a premium, reducing the coin supply and, therefore, pumping the brakes on inflation.

To provide some type of decentralized governance, much like MakerDAO, a secondary token (like MakerDAO’s MKR token) could allow token holders to vote on the governance of the CBDC issuance system, including which types of assets would be needed to mint the CBDC, minimum collateralization ratios for minting new CBDC coins, how transaction fees are measured, how block rewards are issued, and other important governance issues.

While this system could operate on a one-token, one-vote system, whales could dominate this governance system, leading to many of the problems we currently see in ordinary central bank fiat currencies.

To create a more democratic and equitable governance model, a country’s central bank could issue Soulbound Tokens (SBTs). These tokens cannot be transferred from one wallet to another and can be used to verify individual identities. In this model, a Soulbound Token could be issued to every citizen eligible to vote, allowing ordinary people to have a direct say in their government’s monetary system.

While this type of central banking (or rather, decentral banking) might be far off, it does give us a glimpse into what a more decentralized, more democratic financial system could look like in the future.

In Conclusion: CBDC Mining (Or Staking) May Never Happen, But It Opens Up A Variety Of Interesting Questions

In the end, CBDC mining or staking is unlikely ever to occur– at least in the near future, as government central banks will likely want to retain a high degree of control over monetary policy. If central bank fiat currencies are ever replaced by decentralized, blockchain-based currencies, it’s far more likely that independent, asset-backed stablecoins will slowly take market share away from fiat currencies, particularly if they can effectively resist inflation. However, the concept of CBDC mining still remains an interesting idea, at least as a thought experiment– and who knows? Perhaps, one day, it will come to pass.

References:

- Seth, S. (Apr. 2023) What Is a Central Bank Digital Currency (CBDC)? Investopedia.

- Baker, B. (Mar. 2023) What is Bitcoin mining and how does it work? Bankrate.

- (Sep. 2023) Bitcoin Energy Consumption Index. Digiconomist.

- Huestis, S. (Jan. 2023) Cryptocurrency’s Energy Consumption Problem. Rocky Mountain Institute.

- (Jun. 2022) MakerDAO: What Is It and How Does It Work? Real Vision.

- Sergeenkov, A. (May 2023) What Are Soulbound Tokens? The Non-Transferrable NFT Explained. CoinDesk.

- (Sep. 2023) MakerDAO – DefiLlama. DefiLlama.

RECENT POSTS

뉴스, 인사이트 및 더 많은 정보를 받으세요.

뉴스, 업데이트, 업계 인사이트 등 다양한 정보를 받으시려면 Supra 뉴스레터에 가입하세요.

©2026 Supra | Entropy Foundation (스위스: CHE.383.364.961). 판권 소유