Blockchain and Automation: The Complete Guide

July 03, 2023 - 11 min read

Blockchain, Automation, and AI Can Benefit Both Traditional and Crypto-Native Organizations

In today’s world, many organizations, including corporations, non-profits, and governments, still rely on manual processes to organize data and workflows. While the automation of business processes has grown rapidly over the last few decades, traditional automation solutions still have a variety of weaknesses that can slow down organizations and stop them from reaching their full potential.

Whether an organization is transitioning from manual processes to automation or simply wants to improve how they automate processes, blockchain technology has the potential to significantly enhance process automation across a wide scope of industries. This is primarily because blockchain tech effectively removes third-party middlemen through the use of self-enforcing smart contracts, which enhances data security, prevents fraud, and speeds up organizational processes, including compliance and regulatory requirements. In addition, blockchain tech can is often less expensive than traditional enterprise software solutions and can help organizations transition from using multiple types of software to a a single shared (and highly secure) ledger.

As we’ll discuss later, in addition to using blockchain automation for traditional companies, blockchain automation solutions can also be extremely helpful for crypto or blockchain-native organizations. As automation processes and AI continue to improve, automation may play an increasing role in improving security standards across the industry– making crypto safer for average users and bolstering the reputation of an industry that sometimes struggles with its public image.

Blockchain Automation Can Help Improve Processes Across Many Industries

While blockchain automation can benefit organizations in almost any industry, there are a few industries where the technology may be especially useful. Some of these include:

- Transportation and Supply Chain Management: As the world economy has grown more interconnected, supply chains have grown ever more complex– and while that has led to significant economic growth and new opportunities, that complexity also often leads to inefficiencies. By automating processes via blockchain technology, each supplier or vendor across an entire supply chain can verify the exact amount of goods or services they have provided, eliminating paperwork and preventing fraud and counterfeiting.

- Financial Services: While the massive growth of the cryptocurrency market might make it appear that the financial applications of blockchain tech are only appropriate for crypto-native organizations, the reality is far different– and in many cases, legacy financial organizations may have even more to gain from blockchain tech than their Web3 cousins. Blockchain tech is already being used to speed up and automate interbank settlements through protocols like the Ripple blockchain. Stock exchanges, such as the Australian Stock Exchange, have also tested blockchain tech as a way to make transactions faster and more secure. Consumer payments are also another area of interest, and companies like Visa are considering utilizing blockchain tech for both traditional and cryptocurrency transactions.

- Food and Agriculture: The food and agriculture sector is one of the industries most ripe for disruption via blockchain automation. Industry giants like Walmart have taken major strides to introduce blockchain tech into nearly every stage of their supply chain. Using blockchain automation, food and agricultural firms can track fish, meat, and produce back to its place of origin, and can even narrow down items to specific production batches. This can be extremely helpful when preventing food contamination issues like bacterial outbreaks. It can also help companies simplify and streamline their agricultural supply chains, saving precious money and time. Due to this increased level of information, the information gleaned from blockchain automation can also position firms to make better choices regarding the sustainability of their operations.

- Government: From assigning government contracts to voting to getting a driver’s license, many governmental processes still rely on pen, paper, and mail– and that makes things slow and inefficient for everyone involved. Governments may be resistant to bring legacy processes online due to security risks, but blockchain tech can easily change that. In the near future, many believe that all types of government documentation, such as driver’s licenses and passports, may exist digitally as NFTs and could be held by individuals in biometrically-locked self-custodial wallets. Such a transition would make fraud nearly impossible while making it easier to add new data to government documents without replacing them or requiring a lengthy renewal process. Larger processes, such as government contract assignment and monitoring processes, could also become far more efficient as records of expenses and payments are kept on a single, shared ledger.

Challenges in Blockchain Automation

If an organization is fully on-board and given enough time, blockchain automation solutions can usually be implemented relatively easily. However, when blockchain automation involves multiple organizations, such as a series of companies that support a single supply chain, things can become more complex. Despite the many benefits of blockchain automation, some companies may not want to spend money or time on creating a solution for what they see as a problem that doesn’t yet exist.

While powerful multinational corporations like Walmart may have the power to require each part of their supply chain to adopt blockchain technology, smaller businesses may not be so lucky. In these cases, companies may want to switch to new suppliers, but finding suppliers that use compliant blockchain technology may also be challenging. Therefore, many companies may have to wait until their supply chain partners adopt blockchain tech; however, this doesn’t prevent them from reaping the many benefits of adopting blockchain technology internally.

When it comes to adopting blockchain automation solutions, choosing the right solution may also be a tough nut to crack. Enterprise blockchains offer different levels of security, efficiency, and ease of use, and new solutions are being developed daily. Smaller companies or those looking to adopt blockchain tech quickly may lean toward less expensive solutions that don’t require hiring a bunch of blockchain engineers and provide the ability to interface with the blockchain in a low-code or no-code setting.

In contrast, larger organizations, which may require significant customization due to organizational or regulatory requirements, might decide to choose a more expensive, highly customizable blockchain solution. These organizations may be willing to pay the cost of hiring blockchain engineers or a group of outside consultants to ensure their blockchain tech meets their unique requirements.

Finally, when it comes to implementing blockchain automation solutions, interoperability can also be a major challenge. For instance, even if all the organizations that contribute to a supply chain use blockchain technology, they may be using different forms of blockchain tech. While blockchain bridges may allow transactions on one chain to be represented on another, building these bridges (unless they already exist) can be extremely expensive and time-consuming.

Consortium/Federated Blockchains and Blockchain Automation

As we just mentioned, interoperability can be a major challenge when integrating blockchain automation solutions across multiple organizations. One solution, however, is consortium blockchains, also called federated blockchains. Consortium blockchains are typically built by a variety of organizations in the same industry or sector, which allows them to standardize the technology they use and easily and securely transfer data between multiple organizations. Some of the top consortium blockchains currently include Hyperledger, the Enterprise Ethereum Alliance, R3, BankChain, and IBM Food Trust, which is currently used by major corporations like Walmart, Nestle, and Unilever.

Since multiple organizations in each industry already use each consortium blockchain, it’s significantly easier for a new organization to join and begin using it for both internal data recording and external data sharing. In addition, these blockchains may be easier to use, faster to implement, and more secure, as multiple teams have already worked out the kinks in the technology and know how to deploy it efficiently.

Of course, the potential downside to consortium blockchains is that they may be somewhat standardized, so they may not be the best fit for an organization that needs a highly-customized blockchain automation solution. Of course, some chains are more customizable than others, so this may not always be a pressing issue.

Blockchain Automation and Artificial Intelligence

When deciding which new technologies to invest in, blockchain automation and artificial intelligence often appear to compete for the spotlight. However, in reality, these technologies may bring the most benefit to an organization when they’re integrated into the same digital solution. In a way, AI is already a form of automation– so these technologies can even be seen as two sides of the same coin.

For example, while an immutable blockchain ledger may hold evidence that fraud has occurred in an organization, that doesn’t necessarily mean that the fraud will be exposed and dealt with accordingly. However, if an AI-based pattern recognition algorithm was integrated into the blockchain ledger, the algorithm might be able to detect the fraudulent activity and notify the proper individuals.

In addition to preventing negative organizational outcomes, AI and blockchain automation can also work together to increase organizational efficiencies. For instance, an AI-based algorithm could continuously monitor a blockchain-based supply chain tracking ledger. Through independent research, the algorithm might identify a variety of new solutions, such as utilizing different shipping routes or switching suppliers to reduce travel distances and transportation costs.

Automation Can Also Be Incorporated Into Web3 and Blockchain Native Organizations

While much of this article has discussed the benefits of bringing automation into non-blockchain-native organizations, cryptocurrency, DeFi, and Web3 companies also have much to gain from blockchain automation.

For example, AI automation solutions like ChatGPT are already being used to write (and audit) code, with many examples of the software being equal to (or even superior to) human software developers. While writing accurate, error-free code is important for all types of organizations, it’s perhaps the most important for dApps, including DeFi and GameFi protocols, where a single line of incorrect code could allow a hacker to steal millions– or billions of dollars in cryptocurrency.

For example, according to blockchain data firm Token Terminal, between 2020 and 2022, hackers stole over $2.5 billion through vulnerabilities on cross-chain bridges alone.

And, in February 2022, a single security flaw in the Solana-based DeFi platform Wormhole allowed hackers to steal around $325 million.

While some thefts do result from manual or human errors, such as stolen multi-sig private keys, automation processes built into smart contracts could be triggered as a result of suspicious activity, potentially preventing (or time-locking) large withdrawals from wallets by requiring multi-sig signers to provide additional biometric identification, or by implementing other advanced security solutions.

In addition to preventing theft, blockchain automation solutions can also be used to help identify and prevent instances of money laundering, as well as speed up the process of important transparency measures, such as proof of reserve audits, which have become incredibly important to exchanges in the aftermath of the meltdown of exchanges like FTX and crypto lenders like Celcius.

Big Business is Already Adopting Blockchain Automation, But Small Businesses May Not Yet Realize Its Benefits

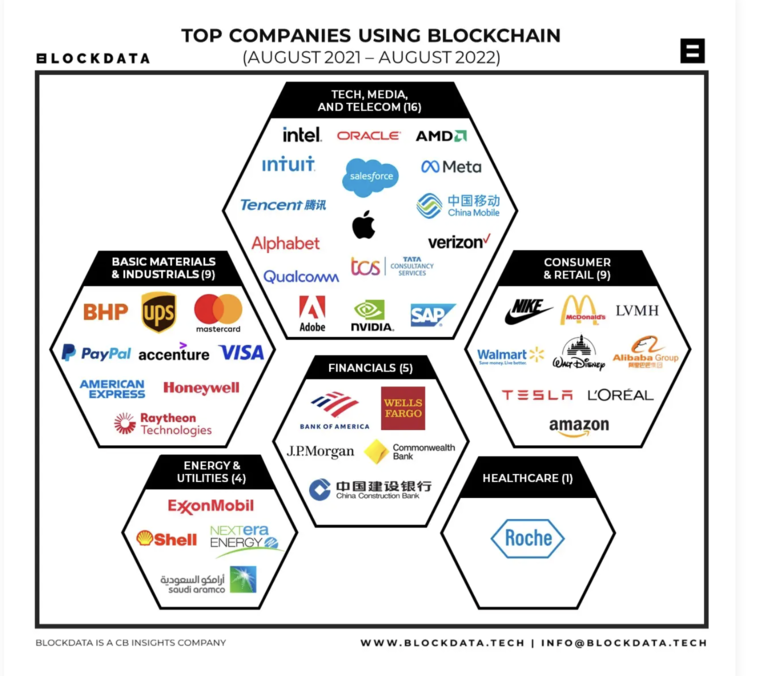

Blockchain automation isn’t just beneficial for big companies– it can also be beneficial for small businesses. As early as 2021, a study showed that 81 of the world’s top 100 companies were actively engaged in blockchain research. 36% of these firms were in tech, telecom, and media, 20% were in basic materials and manufacturing, 20% were in consumer and retail, 11% were financial firms, 9% were energy and utility companies, and 2% were healthcare firms.

Some top companies actively using blockchain tech include Meta (Facebook), Alphabet (Google), Oracle, Wells-Fargo, Bank of America, Tesla, McDonald’s, LMVH, UPS, PayPal, Raytheon, Shell, ExxonMobile, and Nvidia, just to name a few. Common operational uses include preventing counterfeiting, supply chains, invoicing, payment, and receivables management, forex transactions, and the tracking and prevention of intellectual property theft.

However, despite this flurry of blockchain adoption by large companies, smaller businesses have been somewhat slower to jump on the bandwagon. This may be due to the potential expense of implementing blockchain automation, but could also be due to a lack of knowledge.

One of the most impactful areas where small businesses can utilize blockchain automation is in the field of cybersecurity. Around 43% of cyberattacks target small businesses, so this is certainly a pain point for many smaller companies.

But how can blockchain improve small business cybersecurity? One way that blockchain can improve digital security is by replacing the system of manually creating and storing traditional passwords. Instead, small businesses can use automated blockchain-based authentication systems that require digital signatures. By using public key cryptography (just like crypto wallets), these systems can make hacking and intrusion nearly impossible, preventing cyber threats before they start.

However, cybersecurity isn’t the only way that small businesses can benefit from blockchain automation. Businesses engaged in international trade may wish to use fast, cheap, and secure blockchain settlement systems (like Ripple) for international payments, as these payments have traditionally been perceived as higher risk, and often include expensive fees and longer wait times when compared to domestic payments.

However, blockchain automation solutions aren’t just beneficial for traditional small businesses in developed countries; they can also positively impact micro-businesses in developing nations. For instance, many individual and family farmers in Africa are cut off from the traditional financial system and have difficulty selling their products at fair prices. Blockchain tech can enable these types of small business owners to open a wallet for free, use automated stablecoin payment systems, and even connect with larger food distributors to get a fairer price for their goods. This process eschews the manual bureaucratic processes and mandatory minimums required to open traditional bank accounts while preventing theft and fraud.

Blockchain Automation Has Lots of Potential— And We’re Only Seeing The Beginning

With its immutable ledgers and self-enforcing smart contracts, blockchain is an ideal solution for automating processes across a wide scope of industries. Whether a company deals in food, IT services, or luxury goods, blockchain tech can help companies keep more accurate records, avoid fraud, improve operational efficiency, and streamline supply chain management.

As discussed, however, automation can also be essential to blockchain and crypto-native companies and protocols. Automated AI protocols can check blockchain code for bugs to prevent hacks, as well as notify company leaders or outside authorities of suspicious transactions to prevent scams, money laundering, and other nefarious activities.

By providing the industry’s most cutting-edge oracle services, SupraOracles is at the forefront of blockchain automation. Via its high level of security and randomization, SupraOracles can provide companies and projects with the fastest, most secure, and most accurate data possible, allowing them to keep scrupulous records while making operational decisions quickly and decisively. By integrating with 30+ blockchains, SupraOracles also offers the pinnacle of interoperability. So, whether you’re a TradFi company looking to improve your data speed and accuracy, or a DeFi protocol looking to prevent hacks and oracle manipulation, SupraOracles can help your organization thrive.

References:

- What is XRP cryptocurrency, and how does it work? Cointelegraph.

- Chapman, S. (May 2020) Walmart urges its suppliers to use IBM blockchain technology. SupplyChain.

- Anwar, H. (Feb. 2021) Blockchain Consortium: Top 20 Consortia You Should Check Out. 101 Blockchains.

- Tung, L. (Jan. 2023) ChatGPT can write code. Now researchers say it’s good at fixing bugs, too. ZDNET.

- Pereira, A. (Dec. 2022) Bridge attacks will still pose major challenge for DeFi in 2023 — Security experts. Cointelegraph.

- Faife, C. (Feb. 2022) Wormhole cryptocurrency platform hacked for $325 million after error on GitHub. The Verge.

- (Oct. 2022) The Top 100 Public Companies Using Blockchain in 2022. Blockdata.

- Baker, L. 6 Blockchain Applications That Any Small Business Owner Can Use. CloudTweaks.

- (Jan. 2022) How blockchain accelerates small business growth and development. World Economic Forum.

RECENT POSTS

Recibe noticias, información y más.

Suscríbete al boletín de Supra para recibir noticias, actualizaciones, análisis de la industria y más.

©2026 Supra | Entropy Foundation (Suiza: CHE.383.364.961). Todos los derechos reservados